Blog

6 Insurance Data Enrichment Tools to Try

By: Stefan Gergely -

07 March 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

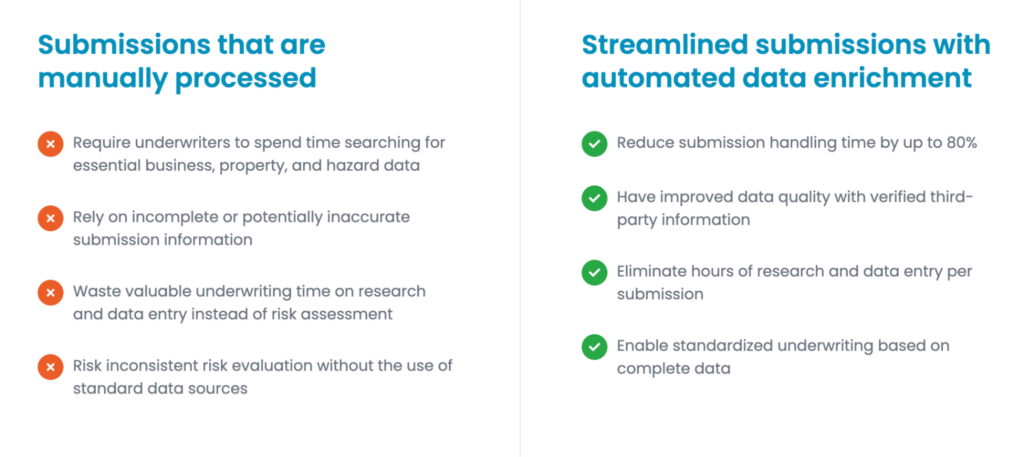

You’re reviewing a commercial property submission when you notice something is off.

The business classification seems too generic.

The revenue figure doesn’t match industry norms. And the location data is three years old.

Without accurate, comprehensive data, you’re left guessing whether this risk fits your tolerance or if you’re pricing it correctly.

Data enrichment tools solve this problem by automatically filling these gaps with verified, real-time information from external sources.

They transform incomplete submissions into complete risk profiles, helping you make confident underwriting decisions faster.

Today, we’ll examine six platforms built for insurance data enrichment, breaking down what makes each one valuable and how they can strengthen your underwriting operations.

When you’re underwriting commercial risks, broad industry classification codes only tell you part of the story.

A manufacturer could be producing organic cosmetics or industrial chemicals, each carrying vastly different risk profiles.

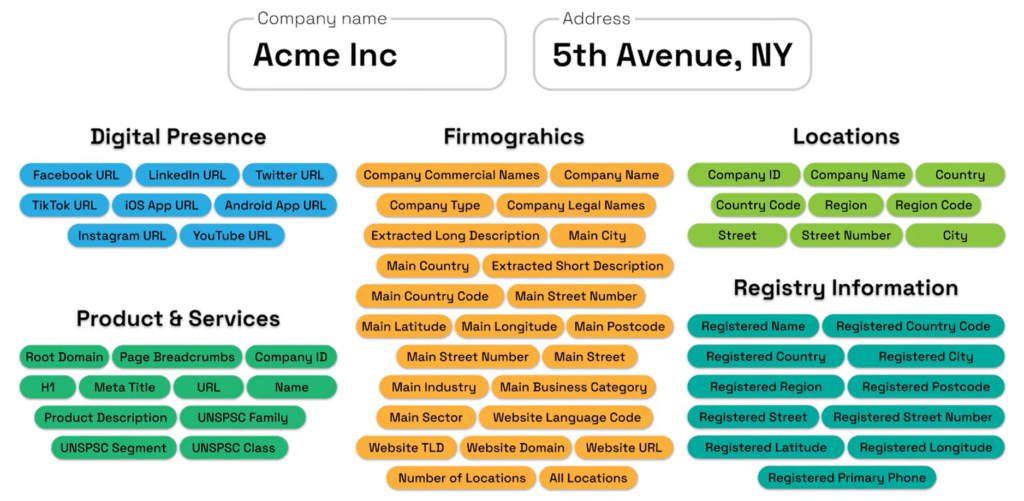

Veridion addresses this gap by delivering AI-powered business intelligence designed for commercial insurance underwriting.

The platform maintains a database covering over 134 million companies globally, with weekly updates to ensure your risk assessments are based on current information.

What sets Veridion apart is depth.

Our database covers:

Source: Veridion

Instead of just knowing that a company manufactures chemicals, you learn which specific chemicals, what safety protocols they follow, and whether they have environmental compliance issues.

This directly impacts underwriting accuracy.

When evaluating a manufacturing subsidiary, Veridion maps the complete corporate hierarchy and ownership structure.

Source: Veridion on YouTube

If you’re insuring what appears to be a small regional operation, you might discover it’s actually part of a multinational conglomerate with substantial additional exposure across your book.

Ultimately, this helps you assess total interconnected risks, rather than treating each entity in isolation.

The Match & Enrich API capability requests in under two seconds.

This speed enables real-time enrichment during quote processes without introducing delays that frustrate brokers or applicants.

Source: Veridion

For insurers incorporating climate risk into underwriting, Veridion provides something most business data providers don’t: actual ESG performance data, not just stated commitments.

You can see which companies have documented carbon reduction programs versus which ones just publish sustainability reports.

You can also identify environmental violations, labor issues, and governance red flags.

Source: Veridion

Veridion shows you what a company actually does, who they’re connected to, how they operate, and what risks they carry.

During renewal cycles, Veridion’s bulk enrichment processes your entire book of business, helping identify concentration risks you’ve accumulated over time.

You might discover significant exposure to companies in a specific supply chain, or that several seemingly unrelated insureds all operate in the same vulnerable geographic corridor.

What sets Veridion apart from other platforms on this list is its comprehensiveness.

While document processing tools help you extract data and geospatial platforms assess location risk, Veridion answers the fundamental question:

What kind of business am I actually insuring?

Everything else builds on that foundation.

If you’re a commercial insurer serious about business intelligence for underwriting, consider scheduling a data consultation to see how Veridion’s depth of data compares to your current data sources.

While Veridion enriches your data with external business intelligence, your first challenge is often extracting usable data from the chaotic documents brokers submit.

SortSpoke specializes in transforming unstructured insurance submissions into structured data.

The platform processes PDFs, emails, ACORD forms, loss runs, and attachments to extract the data points your underwriters need.

The key difference from fully automated extraction is SortSpoke’s human-in-the-loop approach.

Here’s how it works:

AI handles initial extraction, but humans validate results before data enters downstream systems.

This achieves what SortSpoke describes as 100% extraction accuracy because underwriters catch errors that pure automation might miss.

Think transposed digits in coverage limits or misread exclusions that could create massive exposures.

Source: Sortspoke

For example, consider a complex submission with a PDF application, Excel spreadsheet, loss run report, and email clarifications.

SortSpoke processes all simultaneously, extracting relevant data and flagging inconsistencies between documents.

If the PDF states $5 million in coverage but the email references $2 million, the system surfaces this discrepancy rather than silently proceeding with incorrect data.

This validation matters because the extraction errors compound, and a single error can cascade into significant financial exposure or regulatory issues.

Once extracted, SortSpoke’s data enrichment capabilities connect to external data providers, automatically appending firmographic data, property characteristics, and hazard information from your existing vendor relationships.

This integration means submission data gets both extracted and enriched in one workflow.

For underwriters drowning in submission volumes, the efficiency gains are substantial.

What might take 45 minutes of manual data entry happens in minutes, allowing underwriters to focus on actual risk assessment rather than administrative data handling.

Source: SortSpoke

Implementation typically happens within weeks and requires minimal IT resources, making it practical for insurers needing automation without lengthy enterprise software deployments.

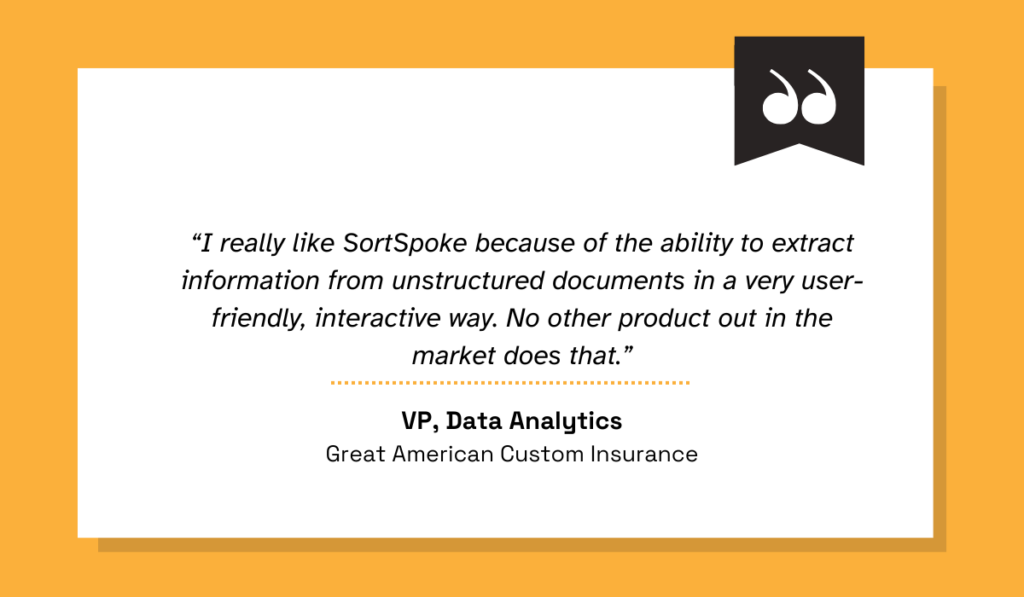

As one AVP of Data Analytics noted:

Illustration: Veridion / Quote: SortSpoke

By combining AI-driven extraction with human validation, SortSpoke ensures data accuracy while drastically reducing the time underwriters spend on manual entry.

This approach not only minimizes risk from errors but also streamlines workflows, letting insurers focus on assessing and pricing risk rather than wrestling with documents.

While SortSpoke handles document chaos and Veridion provides business intelligence, property insurers face another critical challenge: understanding location-based risks at scale.

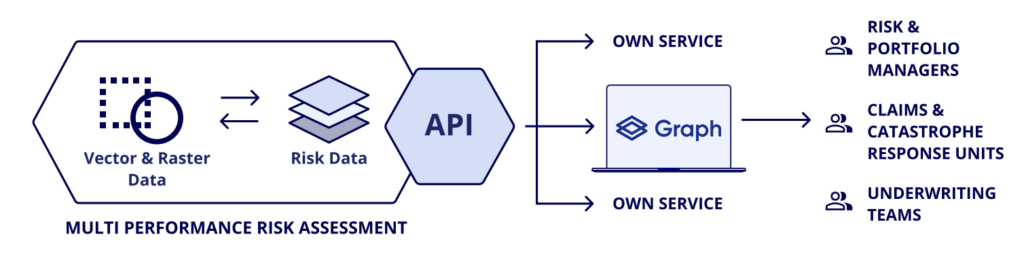

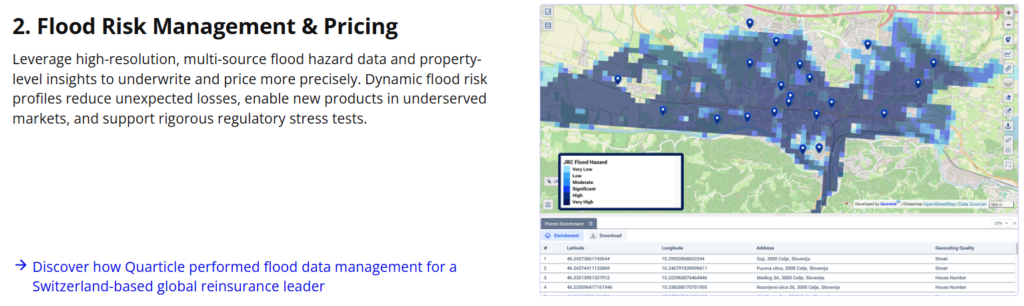

Quarticle’s RAPID platform focuses exclusively on geospatial intelligence for property insurance.

Source: Quarticle

Underwriters use it for property risk evaluation, portfolio accumulation monitoring, and catastrophe exposure analysis.

The platform integrates property boundaries, natural hazard zones, socio-demographic data, and catastrophe model outputs into a unified environment.

This eliminates manually gathering geospatial information from multiple sources and reconciling inconsistent data formats.

That’s a process that can take hours per complex property when done manually.

Source: Quarticle

For individual property underwriting, RAPID provides instant location intelligence.

It’s simple:

You enter an address, and the system returns flood exposure, wildfire risk, earthquake zones, and proximity to other insured properties.

The platform validates addresses, geocodes them precisely, and returns relevant peril scores automatically.

This catches issues brokers often miss, like properties claimed to be “outside the flood zone” that actually sit within FEMA Special Flood Hazard Areas.

Source: Quarticle

But RAPID’s real strength emerges at the portfolio level.

The system analyzes thousands of properties simultaneously, helping you understand geographic concentrations and aggregate exposures that aren’t apparent when evaluating properties individually.

This becomes critical during a catastrophe response.

When a major event occurs, you need to identify affected properties and calculate potential losses immediately, not over several days of manual analysis.

RAPID enables real-time catastrophe modeling, helping you estimate claims exposure while events are still unfolding and providing crucial information for reinsurance notifications and reserve setting.

The platform also supports underwriting workflows by automating routine geospatial checks.

Instead of underwriters researching flood zones and wildfire boundaries manually for each submission, RAPID handles this automatically, reducing processing time and eliminating the human error that occurs during repetitive tasks.

Overall, if you’re a property and casualty insurer managing geographic concentrations across multiple markets, consider evaluating RAPID, particularly if catastrophe exposure management is a priority.

The platforms we’ve covered so far each solve specific enrichment challenges: business intelligence, document processing, and geospatial analysis.

But what if you need a comprehensive platform that orchestrates all these data sources while streamlining your entire risk intake process?

Cytora provides an AI-powered digital risk processing platform that transforms how commercial insurers handle submission data from intake through decision.

Source: Cytora

The platform addresses a fundamental challenge: risk submissions arrive in diverse formats, each structured differently.

Cytora standardizes this varied input into structured, decision-ready risk data.

What distinguishes this one from simpler extraction tools is its reasoning capability.

The platform explains its classification logic in natural language, showing underwriters why it categorized a risk a certain way and which data informed the decision.

Source: Cytora

Instead of receiving a risk class code with no explanation, underwriters see:

“Classified as manufacturing, hazardous materials based on NAICS code 325120, hazmat shipping records from the DOT database, and OSHA incident history.”

This transparency builds trust rather than treating AI as a black box.

This reasoning proves especially valuable when explaining underwriting decisions to brokers, management, or regulators.

You’re not simply stating “our system declined this,” you’re explaining “our system identified elevated explosion risk based on specific operational factors.”

Cytora partners with leading data providers—including Veridion—and orchestrates which sources to query based on the specific risk being assessed.

Source: Cytora

Rather than calling every data vendor for every submission, the system intelligently routes requests.

A restaurant submission might trigger food safety inspection data, while a manufacturer triggers environmental compliance checks, all automated based on risk characteristics.

The platform offers low-code configuration, allowing underwriting operations teams to design workflows without depending on IT resources.

When your tolerance changes or you add a new product line, underwriting managers can modify data requirements and routing logic themselves rather than submitting IT tickets and waiting weeks for changes.

This operational flexibility becomes critical in dynamic markets.

When you need to tighten underwriting criteria for a specific risk class or add new data checks based on emerging exposures, you can implement changes immediately rather than being constrained by rigid system limitations.

Commercial insurers processing diverse submission types across multiple lines should evaluate Cytora, particularly if you need a comprehensive platform rather than point solutions.

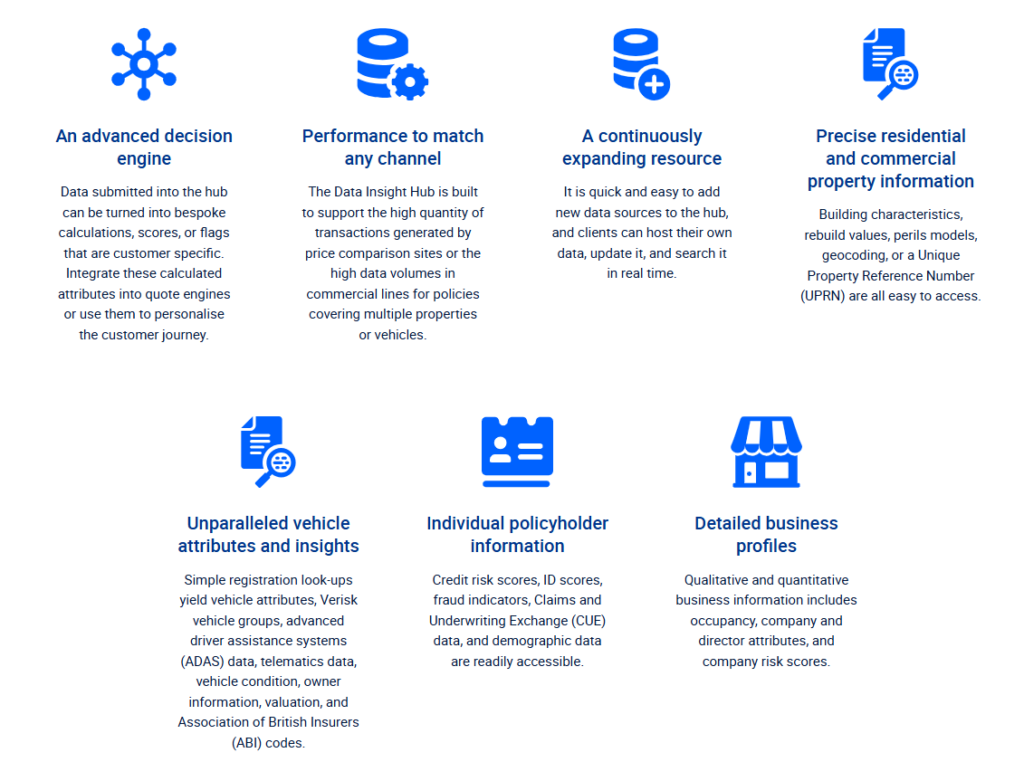

Verisk’s Data Insight Hub consolidates access to multiple insurance data sources through a single API platform.

It addresses the operational complexity of working with numerous data vendors that each require separate integrations.

Source: Verisk

For property insurance in the UK and Ireland, the platform offers comprehensive coverage with building-level data across millions of addresses, including:

This geographic focus means deeper, more accurate data for these specific markets compared to global platforms.

The enrichment operates in real-time during quote processes, directly impacting conversion rates.

When applicants enter an address, Data Insight Hub returns property characteristics, hazard scores, and demographic information instantly, reducing form abandonment by eliminating manual data entry that causes applicants to leave.

Source: Verisk

Commercial property enrichment combines business occupancy data, company information, and business risk indicators with property data to create detailed risk profiles without requiring you to orchestrate multiple data sources manually.

A key operational advantage is flexibility.

Insurers can host proprietary datasets within Data Insight Hub alongside vendor data, centralizing all enrichment needs.

This means your internal scoring models and historical data sit beside external vendor data, accessed through the same API infrastructure.

Fenris Digital specializes in data enrichment and predictive scoring specifically for personal lines, small commercial, and life insurance in the United States.

The platform’s US market focus means deeper coverage and more accurate data for American consumers and properties.

Fenris excels at application pre-fill, which directly addresses the conversion problem.

Using minimal input like name and address, the platform auto-populates insurance application forms with verified household data, property details, and demographic attributes.

Source: Fenris on YouTube

This transforms what would be a 10-minute application into a 60-second verification exercise, dramatically improving conversion rates.

Property enrichment includes detailed building characteristics and replacement cost estimates, ensuring policies are neither underinsured (creating coverage gaps) nor overpriced (reducing competitiveness) due to inaccurate valuations.

Source: Fenris

What distinguishes Fenris from pure data providers is predictive scoring.

Beyond factual enrichment, the tool provides propensity to purchase scores, estimated lifetime value, and retention probability.

These predictions help insurers and agents prioritize high-propensity leads rather than treating all inquiries equally, making sales efforts measurably more efficient.

Data enrichment transforms underwriting from manual research into efficient, data-driven decision-making.

The most sophisticated insurers layer these tools strategically.

They start with comprehensive business intelligence to understand what they’re actually insuring, add document processing to streamline intake, and supplement with specialized geospatial or pre-fill capabilities based on their product mix.

But the foundation matters most.

Without accurate, detailed intelligence about the businesses you’re underwriting, even the fastest document processing and most precise location data can’t prevent the accumulation of correlated exposures that only become visible during claims events.