Blog

6 Types of Concentration Risks Organizations Should Monitor

By: Auras Tanase -

09 April 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

Key Takeaways:

What if your entire company stopped because one person got sick? Or one supplier got hacked?

These are all examples of concentration risk.

It happens when your business relies too heavily on a single thing, whether that’s a supplier, a customer, a region, or a single piece of tech.

In the past few years, companies have collapsed or lost billions because they didn’t see the invisible risk poised by concentration.

But you can.

This article walks through six distinct types of concentration risk. You will learn how to spot them, why they compound, and how to avoid them.

Supplier risk concentration happens when a large share of critical supply flows through a small number of suppliers, locations, or operational choke points.

This risk can stay invisible during stable periods.

But when a single supply chain carries too much weight, even a short disruption can freeze operations on a large scale.

That is exactly what happened in October 2024, when dockworkers represented by the International Longshoremen’s Association went on strike across the US East and Gulf Coasts. Container cranes stopped operating from New England to Texas almost simultaneously.

The shutdown affected 36 ports that together handle 57% of US container volume and nearly one-quarter of total US trade, worth roughly $3 trillion per year!

With so much supply concentrated in the same ports (and workforce), there was no easy rerouting.

llustration: Veridion / Quote: c&en

The chemical industry was hit particularly hard. The affected ports handle 90% of US waterborne chemical imports and exports.

In 2022 alone, over $100 billion in chemical shipments moved through these ports. Gulf Coast ports handled 138 million metric tons, while East Coast ports handled another 31 million metric tons.

When both regions stalled simultaneously, the chemical trade was hit by a severe supplier-concentration shock.

Specialty chemical manufacturers warned that prolonged disruption could bring production across multiple downstream industries to a halt, from manufacturing to infrastructure and consumer goods.

The crisis was resolved later, but not without raising questions about how many industries are fully exposed to supplier concentration risk and to what extent.

The case study could make you wonder if you have alternatives to protect yourself from supplier concentration risks.

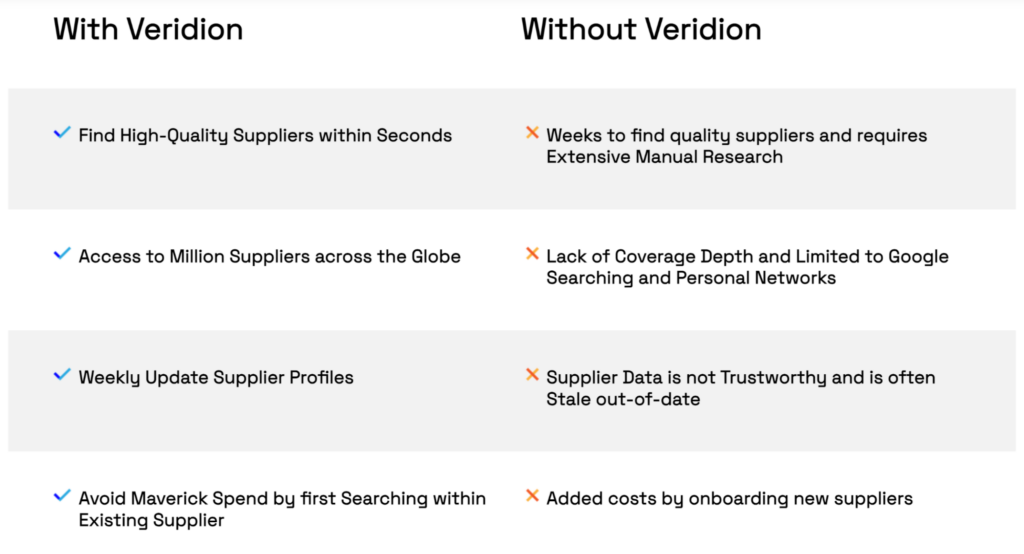

Modern supplier discovery platforms like Veridion can help you here.

The platform uses AI to maintain live profiles on the global supply base: over 130 million companies deep. It tracks critical details like production capabilities, facility types, and corporate hierarchies from a multitude of sources.

Source: Veridion

For a procurement team, this means you can move from asking, ‘Who else makes this?’ to ‘Which qualified supplier in a stable region has the open capacity and financial health to onboard us next quarter?’

It’s intelligence you can truly act on, not just information you can read.

If supplier concentration is hard to see, fourth-party concentration is almost invisible.

Fourth-party concentration risk, by definition, hides behind vendors you don’t contract with but still depend on.

A breach in that single, unseen fourth party can cripple your entire network.

The 2023 MOVEit breach is the definitive example. A vulnerability in one file transfer tool, used by thousands of organizations as a vendor, led to a catastrophic chain reaction.

Over 2,500 organizations and 66 million individuals were impacted. Many victims never had a direct contract with the compromised software provider.

Illustration: Veridion / Quote: CyberSecurity Dive

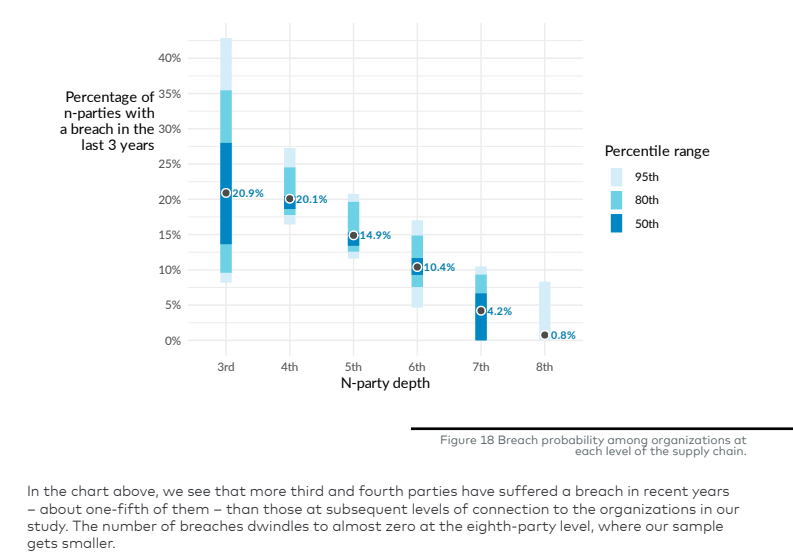

And it’s not just the MOVEit scandal. Research indicates that for every third-party vendor, a company has indirect links to nearly 14 times more fourth and fifth parties.

That creates thousands of unseen dependencies. And not to mention, the risk surface expands exponentially with each new supplier.

Here’s a quick chart depicting fourth-party breaches in comparison to others.

Source: Cyentia

Fourth-party risk is also costlier to clean up. IBM reports the average third-party breach now costs over $5 million. And when it involves a shared fourth party, remediation costs can soar 40% higher due to multi-party complexity.

Traditional questionnaires or annual audits cannot completely defend against this. They may provide a risk snapshot, not live visibility into your vendors’ own dependencies.

Modern defense requires continuous, intelligence-led monitoring. Platforms like Veridion provide this by tracking external threats and exposures across your entire extended vendor network, helping you see the dominoes before they start to fall.

Geographic concentration risk exists when your suppliers, raw materials, energy, or critical inputs are disproportionately located in a single country or region. If that country faces sanctions, conflict, or political disruption, your entire operation can feel the shock.

Europe learned this the hard way.

Before the Russia–Ukraine war, the EU imported nearly 63% of its energy, with Russia as the dominant supplier.

When sanctions followed Russia’s invasion of Ukraine, Europe had no quick replacement. Energy prices and inflation surged, and households faced cost shocks that rippled through every member state.

Some estimates suggest the EU absorbed economic losses of nearly €1.6 trillion, driven by higher energy costs, government subsidies, and slower growth!

The EU paid the cost for over-dependence on one geography.

You can also add the PCK Schwedt refinery case to the context of Russian sanctions.

This refinery, partially Russian-owned and fed by the Druzhba pipeline, supplies 90% of Berlin’s car fuel. It also supplies fuel across eastern Germany and parts of Poland.

But because the refinery is partly owned by Russia’s Rosneft, it makes it a target for US sanctions.

Germany asked for an exemption and got it. But that exemption ends on April 29, 2026.

Source: OilPrice.com

When the U.S. sanctions waiver expires, the refinery’s future is uncertain, directly threatening regional energy security.

A major Polish importer warns there is ‘no way to replace’ its capacity, highlighting a critical failure to diversify supply chains, especially in geopolitically unstable regions.

As you read this, banks, insurers, and suppliers are retreating not because the refinery is unsafe, but because its geography has become a liability.

Generally, geographic concentration is often mistaken for efficiency. And, why not?

Sourcing from one region simplifies logistics and often lowers unit cost.

But today, geography is a risk vector. The question is not whether a region is stable today. It is whether your organization can survive a disruption in that region tomorrow.

Monitoring geopolitical signals and qualifying suppliers in alternative geographies are non-negotiable for foolproof risk management.

Your company might use dozens of different software vendors. That feels diversified, right?

But don’t you think there’s a catch?

What if they all run on the same few pieces of underlying infrastructure? And what if that infrastructure fails for any reason? That’s tech concentration risk defined.

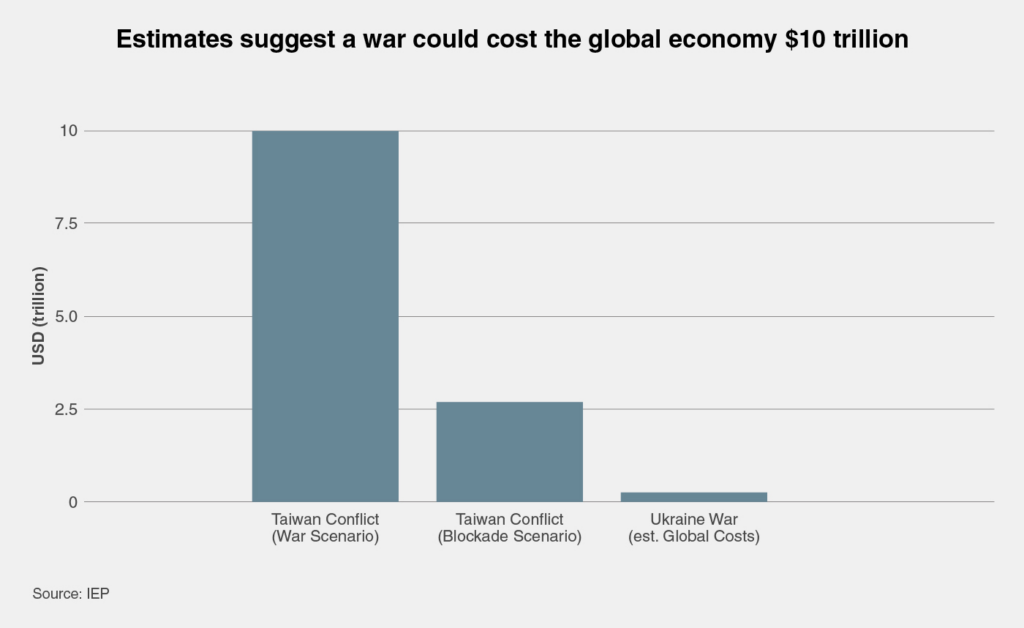

The global semiconductor supply chain is an apt example here.

TSMC controls about 70% of general chip manufacturing and produces roughly 90% of the world’s most advanced chips used in AI.

Any disruption in Taiwan (imagine a China-Taiwan war) would halt production globally, shaving trillions of dollars from economic output and freezing manufacturing across many top companies and sectors.

Source: Vision Of Humanity

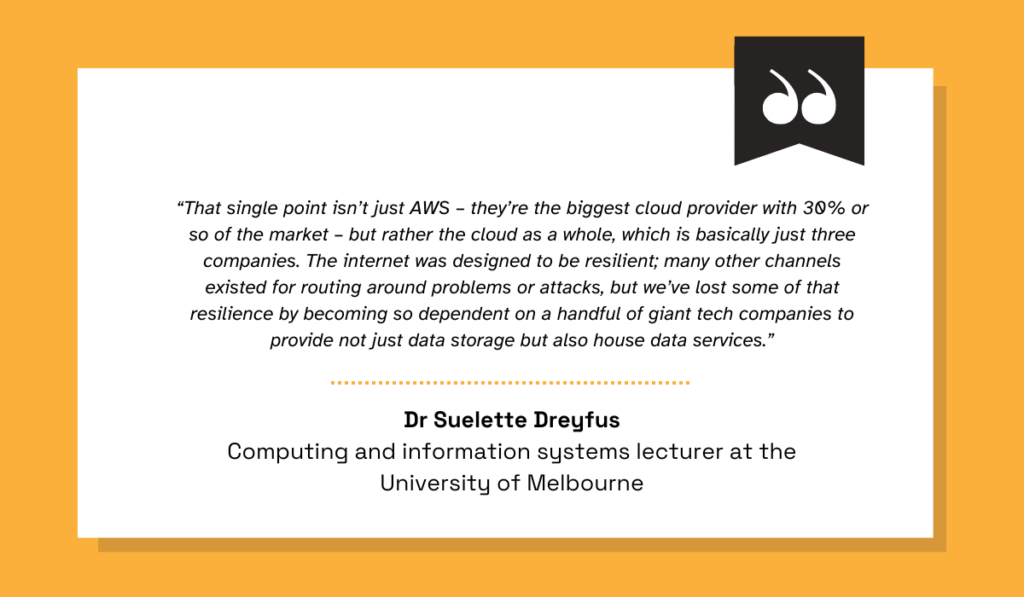

This pattern repeats in cloud computing.

Amazon Web Services, Microsoft Azure, and Google Cloud collectively control about 75% of the cloud infrastructure market. And a failure in one can create a global domino effect.

For instance, in October 2025, a bug in an AWS automation system triggered a multi-hour outage. It disrupted over 2,000 companies, including major platforms like Signal, banking sites, and Duolingo, generating 8.1 million user problem reports!

Illustration: Veridion / Quote: The Guardian

Technological concentration is particularly dangerous precisely because it feels like diversification. Or at least gives the illusion of diversification.

The solution is not to abandon dominant platforms. That is neither practical nor productive.

The best thing to do is to identify which of your dependencies are concentrated and map the infrastructure under your vendors.

Ask what happens if a TSMC or AWS experiences a prolonged failure. If the answer is ‘we stop,’ then you know that you have exposure and need more diversification.

| 🙂 Fun Fact: Taiwan’s semiconductor industry generated roughly $165 billion in revenue in 2024. That’s nearly 1/5th of Taiwan’s GDP! |

Customer concentration risk is the mirror image of supplier risk. Instead of relying on a single source of input, an organization relies on a single source of revenue, and that’s a fragile place to be.

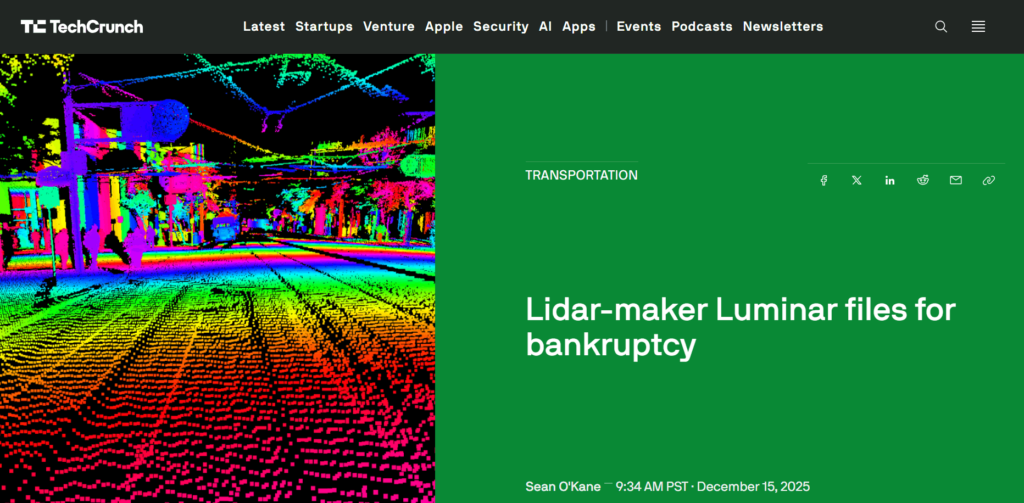

Consider the case of Luminar Technologies.

The company secured early partnerships with both Volvo and Mercedes-Benz, betting these automotive giants would drive mass adoption of its lidar technology.

And for a time, this strategy did work.

Volvo, in particular, became the anchor client, with orders scaling from tens of thousands to a planned 1.1 million units.

Luminar expanded its workforce and manufacturing capacity in line with Volvo’s projected demand. However, when Mercedes-Benz exited the partnership in late 2024 (citing unmet requirements), Luminar was left exposed. Volvo wasn’t just a major client anymore; it effectively was the business.

The collapse was swift once Volvo left. The carmaker terminated its supply agreement, pointing to contractual failures and supply chain concerns. It also demonstrated it could advance its safety features without Luminar’s specific technology.

Luminar Technologies filed for Chapter 11 bankruptcy shortly after.

Source: TechCrunch

Now, you may think that singular government clients cannot be that much of a risk. But the collapse of outsourcing giant Carillion shows otherwise.

The firm derived 45% of its UK income from public projects, with the government awarding it £2bn in contracts even after profit warnings. Its failure with £7bn in debts caused 3,000 direct job losses, endangered 450 public projects like hospitals and schools, and crippled a 75,000-person supply chain.

So, size, reputation, or government backing cannot eliminate customer concentration risk.

Remember that the presence of a large client is not the problem. The absence of a second is. The short-term cost of diversification is almost always lower than the long-term cost of a single exit.

Key-person concentration risk is the organizational dependence on a single individual’s expertise, reputation, or leadership (and a risk that’s not often talked about).

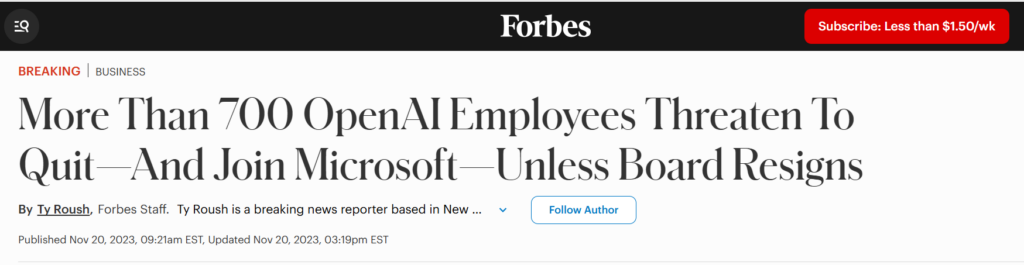

OpenAI faced this concentration risk in late 2023.

Following CEO Sam Altman’s sudden firing, the company faced immediate instability. More than 700 of its roughly 770 employees signed a letter threatening to resign unless the board reinstated him.

This mass exodus would have crippled the AI firm’s operations.

Source: Forbes

Employees openly stated they would move with Altman to Microsoft if needed. Less than a week later, Altman returned as CEO.

The episode exposed how a ‘key person’s’ influence can affect overall corporate stability or even the survival of the company.

The problem in this case was that the entire organization had built itself around a leader to such an extent that its workforce viewed the company and the CEO as inseparable.

Nestlé’s leadership turmoil shows a different angle of the same risk.

In 2025, Nestlé fired its CEO, Laurent Freixe, after an investigation found he concealed a romantic relationship with a subordinate, breaching the company’s code of conduct.

Source: Reuters

It was Nestlé’s second CEO exit in a year. A top investor noted the loss of two CEOs and a chairman in one year was ‘of historic proportions for Nestle.’

Shares dropped during the transition, and it was no surprise that the world’s largest food and beverage company faced falling sales and declining investor confidence during the period.

Key-person risk can be addressed by distributing company leadership in a risk-free manner and not concentrating too much power in one person or department.

Concentration risk isn’t about avoiding countries, people, or partnerships. It’s about avoiding blind spots.

Whether it’s a supplier, a location, a piece of tech, a major client, or a star leader, putting too much trust in one point of contact can backfire big time.

The first step to resilience is simple: see the risk. Map your dependencies, ask the tough ‘what if’ questions, and build intentional buffers.

Not because they predict disruption. But because they assume it will happen.

By doing that, you’re building a stronger, more adaptable business.

Isn’t that the point, after all?