Blog

How Insurance Market Intelligence Creates Competitive Advantage

By: Stefan Gergely -

01 July 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

Key Takeaways:

Insurance fraud costs U.S. consumers $308.6 billion every year. Not because insurers lack data; they have more of it than almost any other industry.

The problem is that most of that data never makes it into the decisions that matter.

It sits in separate pockets within organizations, surfacing for daily operations, but rarely ever being used to inform bigger-picture strategy and build a long-term competitive advantage.

Market intelligence changes the equation.

Through synthesizing clusters of market data into a coherent strategic picture, it gives insurers something worth more than information alone: a genuine edge.

Here’s what that edge looks like in practice.

Traditional actuarial data tells you what happened. Raw, very matter-of-fact, hard to challenge. Information in its purest form.

But it’s not the final form you can use to push your company’s efforts further.

Market intelligence can translate that raw data into much more valuable insights. With a more structured approach to analysis, you can find out what customers want right now.

Today, most clients arrive with expectations shaped by every other industry they interact with.

They expect their insurer to know them not as a statistical profile, but as an individual with specific needs, preferences, and circumstances.

The data backs this up.

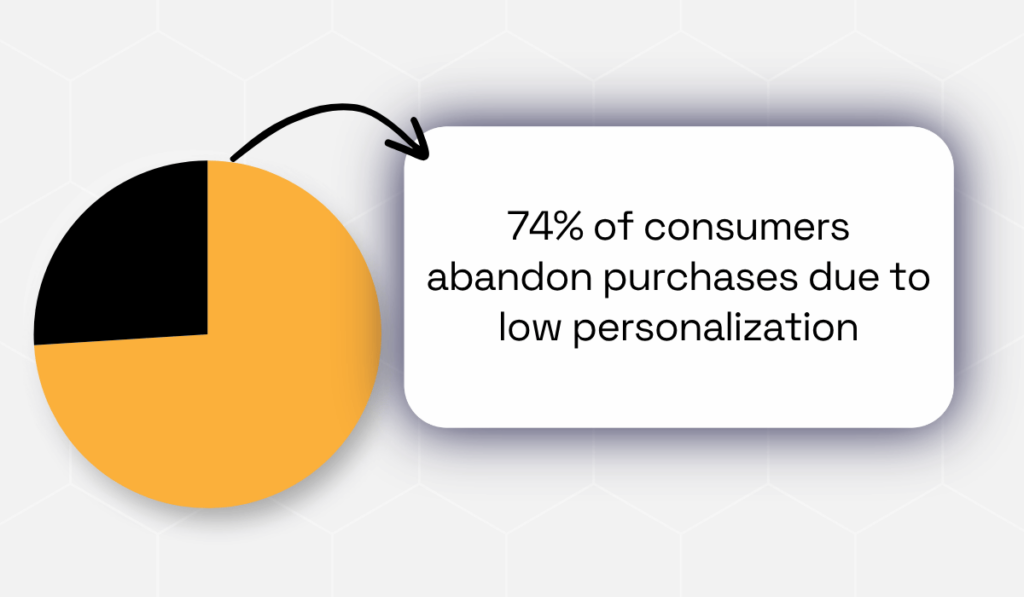

According to Accenture’s “The Empowered Consumer” research report, 74% of consumers have abandoned purchases due to feeling overwhelmed by the noise stemming from ineffective personalization efforts.

Illustration: Veridion / Data: Accenture

Moreover, only 39% believe that companies have their best interests at heart.

The strength of market intelligence comes from its ability to close this gap mindfully.

Those are all sources of pure informational gold that insurers can use to build real-life profiles, not just generic solutions only masquerading as genuine answers to real problems.

Use intelligence to your advantage and uncover gaps, see what drives more churn, and identify segments of your customer base that might be going underserved.

Do it right, and you’ll gain that edge before they take their business elsewhere.

The commercial payoff is significant, to say the least.

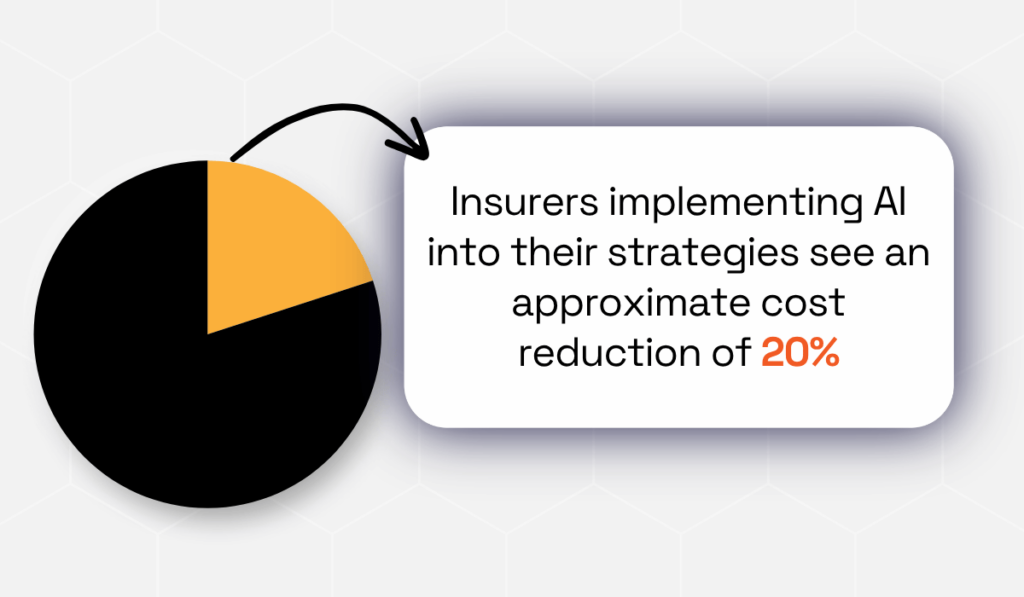

BCG’s 2026 analysis of AI-first insurers shows that data-driven strategies are already unlocking cost reductions of approximately 20%, alongside 3% to 5% gross written premium growth.

Illustration: Veridion / Data: BCG

These are numbers that purely reactive, one-size-fits-all carriers simply cannot match.

Need more evidence?

Look no further than an actual insurer who already implements smarter strategies at an individual level.

Progressive, an insurance company serving over 43 million customers, champions their Snapshot program.

It works by collecting real-time driving data through a telematics device to offer premiums that reflect driver behavior rather than broad statistical categories.

As a result, policyholders with spotless records pay less on account of their skills on the road, while their insurer prices risk more accurately.

What’s critical to underline here, though, is that neither outcome would be possible without the underlying intelligence layer.

That’s the core value: not just knowing who your customers are, but understanding them well enough to actually serve them and benefit both parties while doing so.

Even when you decide to place personalized experiences at the heart of your operation, insurance has, by nature, always been reactive.

Risks emerge; products follow. You can’t anticipate everything.

Or at least, not without a smart implementation of market intelligence.

By spotting emerging risks early and identifying coverage gaps before they become crises, you can give yourself the time to innovate rather than scramble to catch up.

The mechanism is straightforward. You aggregate signals from multiple sources simultaneously:

Mind you, reading these signals alone won’t guarantee a successful product, but what they give you is a pointer that tells you where to concentrate your efforts rather than rely on pure guesswork.

Climate risk is the clearest current example. As extreme weather events grow more frequent and severe, traditional indemnity models have struggled to keep pace.

Günther Thallinger, a member of Allianz’s management board, put it plainly in a 2025 statement on the risks climate change poses to insurers and everyone they cover:

Illustration: Veridion / Quote: Günther Thallinger on LinkedIn

For instance, in February 2025, Swiss Re, Aon and Floodbase joined forces to launch a parametric hurricane solution for businesses along the U.S. Gulf Coast.

Payouts trigger automatically when certain conditions are met, such as wind speeds or storm surge water levels exceeding predefined thresholds.

The product exists because market data made the case: policyholders needed faster, more objective coverage than traditional models could provide.

The gig economy has driven a parallel shift.

As platform-dependent workers have grown in number, so has demand for coverage that matches their actual exposure.

Flexibility became a massive friction point, as the ability to turn coverage on and off by the shift, trip, or job simply didn’t exist.

Insurers who tracked that shift early were positioned to build for it. Those who didn’t, found themselves competing in a market they hadn’t anticipated.

Again, market intelligence doesn’t solve either problem outright. It can’t work miracles.

But, on a smaller scale, utilizing it to your advantage can tell you in advance there are problems that exist beyond your periphery, and that you should address them before your competitors move and your clients follow.

Understanding the market means understanding the competition. In insurance, that means more than knowing who sells similar products.

Competitor strategy plays out across three dimensions simultaneously.

| Pricing | rate adjustments in a specific state or segment reveal how a rival is reading risk and which customers they’re chasing or quietly retreating from |

| Product offerings | New structures, coverage expansions, and benefit modifications reflect deliberate choices about where a carrier wants to compete |

| Promotional activity | It reveals which segments a competitor is prioritizing and how aggressively they’re investing in acquisition |

Tracking all three requires continuous monitoring, not half-hearted periodic reviews.

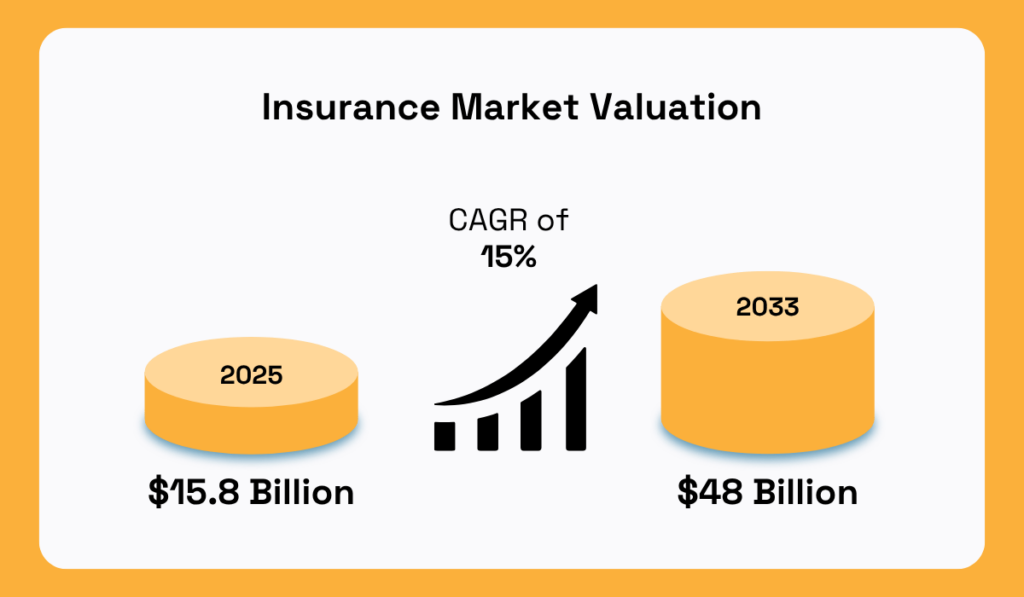

And there are certainly data points to track, as the global insurance analytics market was valued at $15.8 billion in 2024 and is projected to more than triple to $48 billion by 2033.

Illustration: Veridion / Data: Grand View Research

This growth comes courtesy of how fast the insurance market moves.

Rate filings, for instance, are public documents submitted to state regulators all the time, not just on a specified, predictable cycle.

They contain significant strategic signals.

A carrier monitoring them in real time spots a competitor’s rate adjustment the week it happens, not the quarter after, when a research firm publishes a summary.

By that point, the window to respond has already narrowed.

Market intelligence operationalizes this exact process.

Rather than manually assembling a competitive picture from press releases and trade publications, insurers maintain a continuously updated view of competitor positioning and detect patterns in that movement before they become obvious.

Real-time competitive intelligence gives you the ability to respond to any market opportunity quickly because, with visibility, you come up with more thoughtful strategies.

Be it a new product launch or a price change, you can quickly fill a need that arises.

The only requirement is noticing.

Market intelligence is typically framed as an external capability. A tool for understanding customers, tracking competitors, and identifying opportunities.

Close, but that framing isn’t entirely complete. It’s missing one critical idea.

The same data infrastructure that powers external insight also transforms how efficiently an insurer operates internally.

Claims management is the clearest example.

Historically, it’s been one of the most labor-intensive functions in the industry.

Can’t function without manual data entry, regular document reviews, and adjuster judgment applied to unstructured information to make chaotic data parsable.

By making data structured, centralized, and continuously updated, market intelligence gives claims handlers a complete picture from the moment a claim is opened:

All accessible without manual assembly.

In fact, the immediate effect of utilizing data in claims processing is staggering.

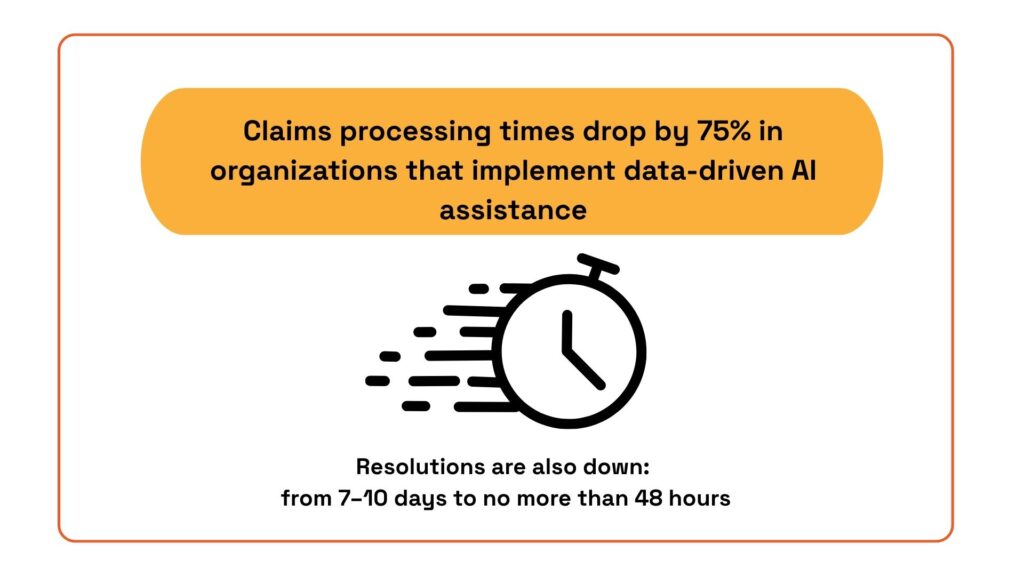

A paper published in the European Journal of Computer Science and Information Technology shows that resolution times dropped by 75% in organizations using data-driven AI assistance, from 30 days to 7.5 days.

Routine claims now resolve in 24 to 48 hours, down from 7 to 10 days.

Illustration: Veridion / Data: European Journal of Computer Science and Information Technology

Underwriting follows the same pattern.

Clean, current intelligence on applicants and risk segments means underwriters spend less time gathering information and more time applying judgment to it.

Here, a telling example comes from Aviva, another global insurer.

After deploying more than 80 AI models across its motor claims domain, the company reported saving over £60 million in 2024.

The intelligence layer is what made that operational gain possible.

And what does the future hold?

Looking ahead, McKinsey analysts indicate that more than 50% of claims activities have the potential for automation by 2030.

Putting all the puzzle pieces together, it should become clear that the more data you channel into your strategy, the higher the ceilings of your operational efficiency.

The $308.6 billion annual cost of insurance fraud in the U.S., as reported by the Coalition Against Insurance Fraud, isn’t just a fraud problem.

It’s a data problem.

Illustration: Veridion / Data: Coalition Against Insurance Fraud

One critical vulnerability that heavily contributes to this figure being so high pertains to the methodology of risk assessment.

Usually, it takes place only one time: when the initial policy is underwritten. Once circumstances change, reviews rarely happen.

But our world remains dynamic and unpredictable.

The policyholder’s environment or financial situation can shift drastically at any moment, creating information asymmetry and making them feel like their insurance isn’t fully adequate anymore.

That often leads them to abuse and fraudulent activity.

None of this slowly-creeping risk reaches the underwriter until it’s too late. By the time anything becomes visible, the damage is usually done.

Market intelligence changes what’s knowable in the interval between those two moments.

External signals, like business activity changes, regulatory filings, or ESG shifts, update continuously well before anything gets reflected in policy.

That gap between signal and disclosure is where proactive risk intelligence operates.

And it’s precisely the problem Veridion’s platform addresses.

Using advanced AI and machine learning to analyze billions of internet pages almost instantly, Veridion identifies changes to business activity, risk exposure, and products and services.

This, in turn, enables accurate premiums and coverage calculations before a policy is mispriced.

Source: Veridion

Our database covers more than 130 million companies globally, updated weekly, tracking operational changes, hidden affiliations, location accuracy, regulatory compliance, and ESG indicators simultaneously.

The result?

A fundamentally different risk posture, where the signal surfaces before the loss, not the other way around.

The insurance industry has never lacked data. What it has lacked is the infrastructure to turn that data into a strategic asset.

This is where market intelligence comes in.

From understanding customers to tracking competitors in real time, detecting risk before it escalates, and driving innovation, the benefits covered in this article share a common thread:

They all move insurers from reactive to proactive.

This type of structural shift needs to be embraced by smart insurers who are willing to put their strategies under the microscope.

Those that do will find gaps they didn’t know existed, and implementing the right solutions in the right spots is where the real competitive advantage lies.