Blog

Why SaaS Companies Can’t Afford to Ignore Competitive Intelligence Anymore

By: Stefan Gergely -

03 July 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

Key Takeaways:

Two SaaS companies start the year shipping the same product to the same customer.

By year-end, one is winning enterprise deals, and the other is fighting to keep its renewals.

The gap between them is rarely about who built the better product.

It comes down to how well a company reads its market, where competitors are heading, and where the next opening is.

Companies that have built a system to read those signals win. Those who haven’t keep guessing and, well, losing.

Here are five reasons competitive intelligence can no longer be optional for SaaS companies, and why it deserves more attention.

Competitive intelligence (CI) sharpens product decisions by showing you where the market is heading, what customers need, and how competitors are evolving.

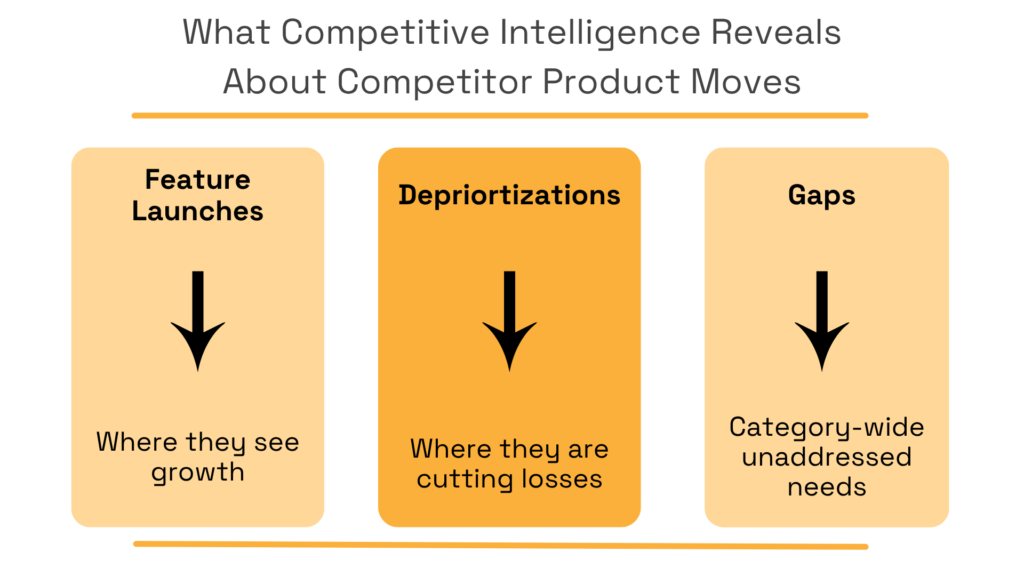

Three categories of competitor signals matter most when shaping a product strategy roadmap.

Source: Veridion

The first is which features competitors are launching. These reveal where they see growth and where they expect to face pressure.

The second is which features they are deprioritizing, since those often expose categories that did not deliver value.

The third is gaps in their offerings. Remember, unaddressed needs in a competitor’s portfolio are often unaddressed needs across the entire category.

In any case, not paying attention to competitors and their products is a mistake.

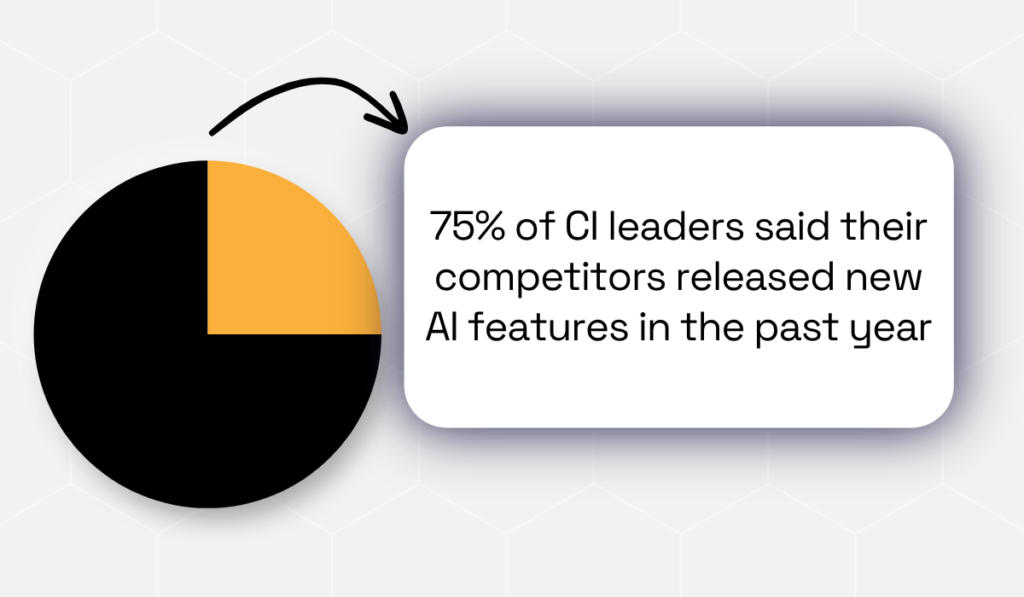

According to What Competitive Intelligence Reveals About Competitor Product Moves, 75% of CI leaders said their competitors released new AI features in the past year.

Illustration: Veridion / Data: Crayon

When that many competitors are moving, building without a competitive context is a risk you can’t afford.

A single competitor signal is interesting. But a pattern across a quarter tells you where the market is going.

The companies that track that pattern, not just the headline, make better roadmap calls.

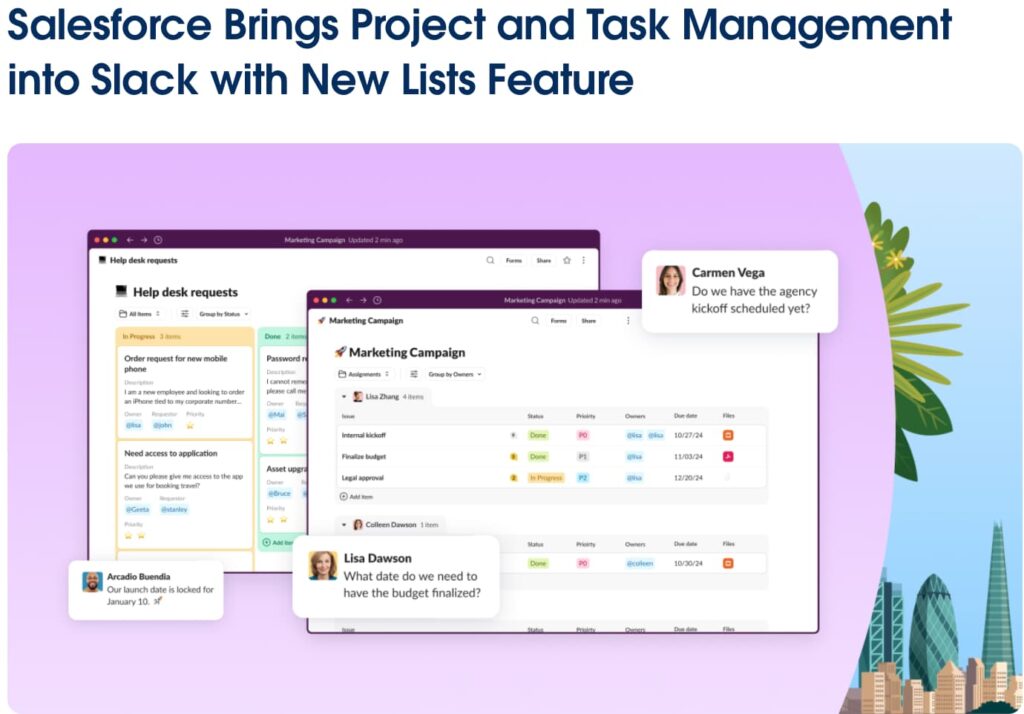

A good example is Slack’s launch of project tracking functionality in mid-2024, moving into a category that dedicated project management software had owned for years.

That move did not come from internal instinct alone.

Slack’s team had spent years watching where users dropped and where adjacent platforms had pulled revenue away.

Source: Salesforce

The launch made sense because they understood what competing project software did well and where it left friction.

Product signals also extend beyond release notes. Hiring patterns and the integrations competitors invest in often tell you where they intend to build long before they ship.

Companies that monitor those signals review their roadmap against current data. The ones that don’t tend to learn the same lessons through lost deals.

Now, the same intelligence also reveals something else, where the market has room to grow.

Studying a competitor obviously tells you where they are. But sometimes, the more useful question is where they are not.

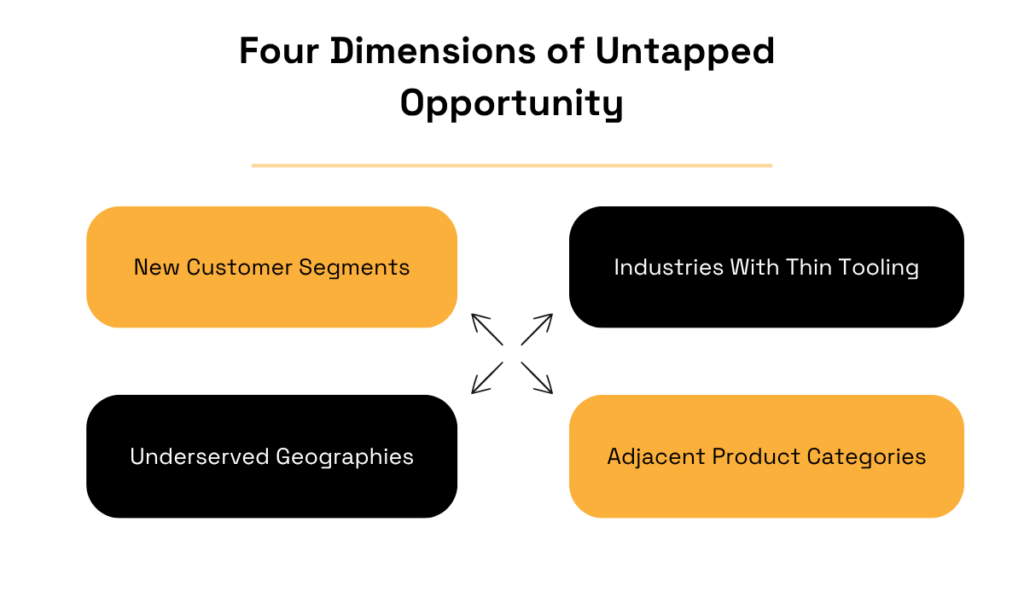

Every SaaS market has an area that competitors have not fully reached, whether that is a customer segment, a geography, or a product category.

The four dimensions below show where those openings most commonly sit across SaaS markets.

Source: Veridion

The companies that get to those zones first capture the most value before the rest of the market crowds in.

Furthermore, each quadrant points to a different kind of opening.

| Type | What It Means? |

|---|---|

| New customer segments | Groups competitors have not segmented for |

| Industries with thin tooling | Verticals where adoption is rising but specialised software is scarce |

| Underserved geographies | Markets where competitors have weak distribution or local feature gaps |

| Adjacent product categories | Use cases where solutions exist, but none are purpose-built for the job |

Competitive intelligence helps you see those zones earlier because it surfaces patterns competitors are not yet acting on.

When a competitor is hiring heavily in one vertical and underinvesting in another, that mismatch points to an opening.

When several competitors describe their roadmaps in similar language but none of them have shipped against it, the category is wide open.

Geographies and segments often move together. A competitor underinvesting in one region is usually also underinvesting in the mid-market accounts.

Reading one signal tends to point directly to the next, which is why systematic monitoring catches openings that one-off research misses.

Notion’s launch of Notion Calendar in January 2024 is a clean example. Calendar software was already crowded with a long tail of standalone apps.

But no one had built a calendar that lived inside the same workspace where teams wrote docs, ran projects, and managed knowledge.

Source: TechCrunch

The opportunity sat in the seam between two saturated markets, visible only to teams watching where existing players were not building.

The bottom line: Being second to an opportunity costs more than lost deals. The early mover locks in the best reference customers and shapes how the category gets defined.

Without competitive intelligence, most companies spot these openings only after a competitor announces the move.

By then, the window is already closing.

Pricing is the most powerful decision a SaaS company makes. Most get it wrong because they make it without any data backing.

Competitive intelligence shows what competitors charge, what they bundle, and where they give ground. It also shows how they tie price to the outcome a customer is actually paying for.

Without that view, your pricing team is guessing.

The 2024 SaaS Benchmarks Report by High Alpha and OpenView surveyed 800+ companies and found that 68% of AI products still run on a subscription model.

Buyer expectations have moved toward outcome-based pricing but most companies still haven’t.

This model prioritizes charging customers based on tangible business results, like closed leads, resolved support tickets, or revenue generated, rather than access or usage.

SaaS companies are still learning how to build such pricing models.

The point is, companies that avoid making changes when the market is shifting around them tend to lose more ground than those that move early.

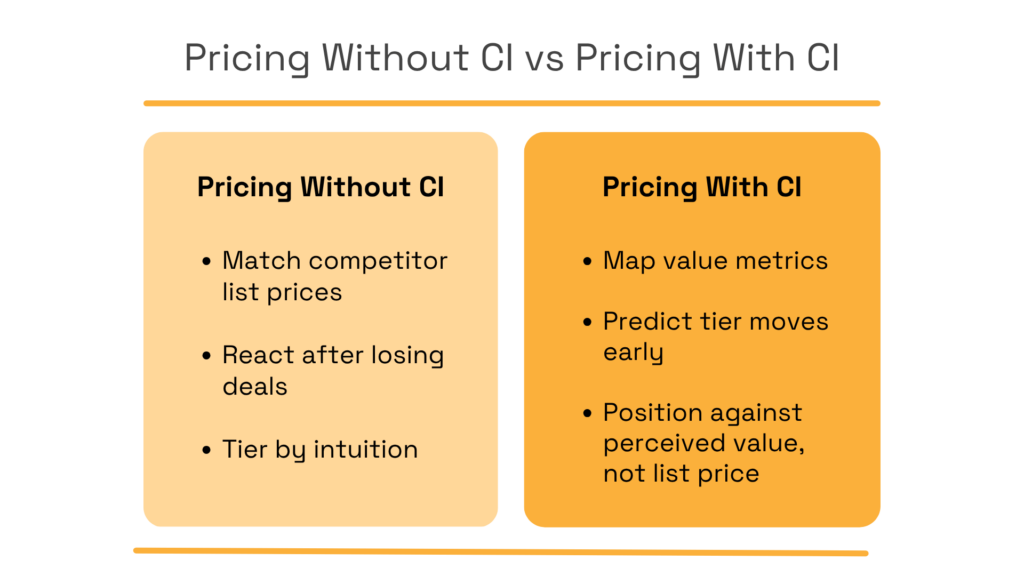

The comparison below shows how that shift changes the quality of pricing decisions in practice.

Source: Veridion

Now, most SaaS leaders default to reading competitor price pages and matching. That is the lowest-value version of pricing intelligence.

It doesn’t answer why competitors packaged it that way, what value metric they are monetizing, and how their pricing maps to how customers actually buy.

But remember: the goal is never to be cheaper. It is to be perceived as offering stronger value at the price you charge.

And that’s why you need CI.

When pricing teams have visibility into how:

…they make sharper choices about which features belong in which tier.

They also flag when a competitor switches pricing models or ties fees to outcomes. Both signal where customer value perception is moving.

The current scramble around AI add-on pricing is a live example.

SaaS companies are testing whether to bundle AI features into existing tiers, charge for them as separate seats, or meter them by usage.

Each model carries different risks.

Competitive intelligence lets pricing teams see who is testing what, how the market is responding, and which positioning is winning.

Those signals live across pricing pages, sales conversations, and review sites all at once. That cross-channel pattern is exactly what a pricing deck built in isolation will never catch.

Pricing is one place where drift shows up. By the time it shows up in churn, the damage is already done.

Customer churn is rarely about a single failed feature.

It is about a slow drift in how your customers value what you sell relative to what your competitors are offering them.

Competitive intelligence catches this early.

It surfaces what attracts your customers to competitors and shifts market expectations. The gaps in your product showing up in switcher rationales are also revealed.

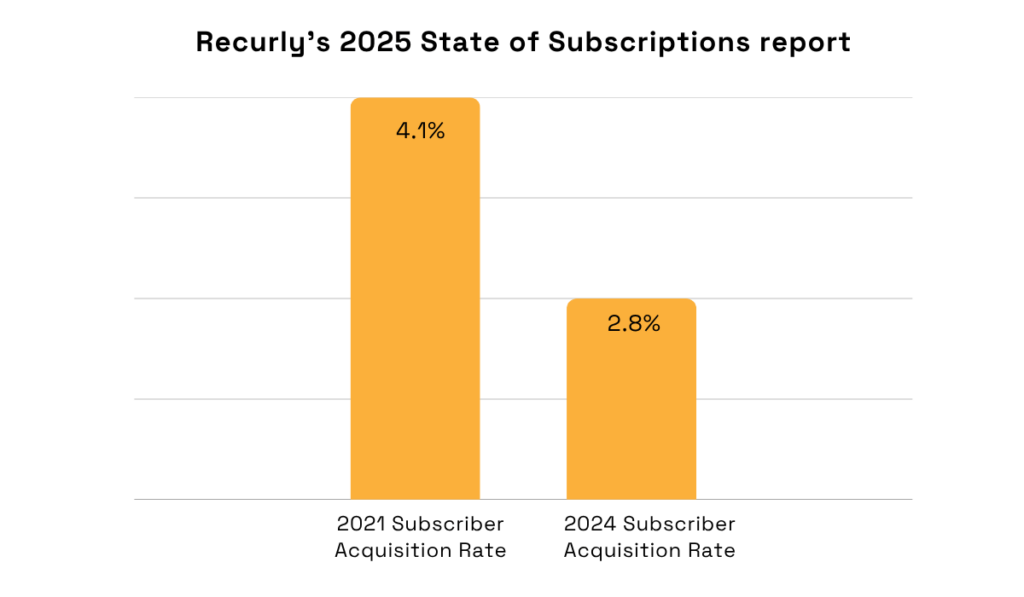

According to Recurly’s 2025 State of Subscriptions report, subscriber acquisition rates across the industry have dropped from 4.1% in 2021 to 2.8% in 2024.

Illustration: Veridion / Data: Recurly

That decline reframes the economics of every SaaS company. When you cannot rely on new customers to absorb churn losses, holding onto the ones you have becomes the main priority.

The thing is: customers rarely leave for the reasons they give your CS team.

The patterns only show up when you look across multiple departures. Something like a missing integration or a competitor shipping AI features faster are a few.

A pricing model that fits how customers use the product can also be one.

Competitive intelligence gives you the aggregate view that lets you intervene before the next account starts looking.

There are three common methods for CI analysis that help combat customer churn:

| Win-loss analysis | When you know which competitor your churned customers moved to, you can map the patterns like shared verticals, shared deal sizes, shared trigger moments |

| Feature parity tracking | When a competitor closes a gap that previously made your product the safer choice, you have a short window to respond before customers start noticing on their own. |

| Messaging drift | When the language competitors use shifts, the language your customers use will shift soon after, and your renewal narratives need to keep up. |

Most retention work runs on lagging indicators like cancellations, NPS dips, and support ticket volume. Competitive intelligence adds the leading ones.

It shows which competitor announcements landed with your customers, which features they are starting to ask about, and which messages are pulling attention away from renewal.

That turns customer success into an early warning system, not the last to know.

Catch it early, and it is a retention problem you can fix. Miss it entirely, and a competitor has already made it their growth story.

Competitive intelligence is, at its core, an early warning system. It identifies threats before they reach the revenue line.

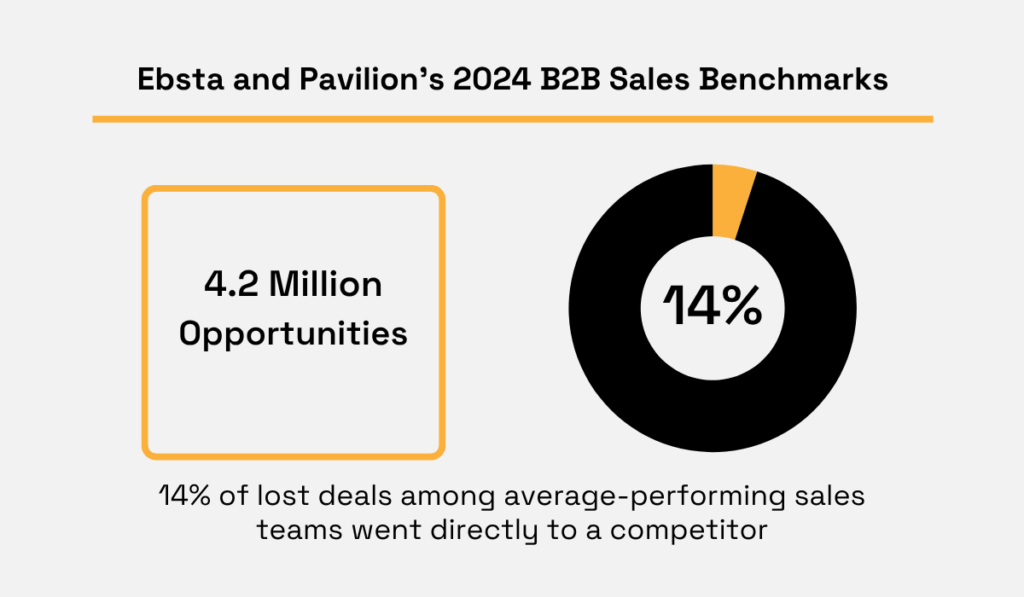

According to Ebsta and Pavilion’s 2024 B2B Sales Benchmarks, out of 4.2 million opportunities, 14% of lost deals among average-performing sales teams went directly to a competitor.

Illustration: Veridion / Data: Ebsta

For every deal a competitor wins outright, several more stall in indecision. It’s because the prospect could not tell which option was right for them.

Real-time competitive intelligence goes beyond periodic monitoring.

The most useful signals cover funding, hiring, product launches, customer announcements, and shifts in commercial footprint, gathered continuously rather than in quarterly snapshots.

The capabilities below show how business intelligence platforms like Veridion structure that kind of intelligence for SaaS teams operating at scale.

Source: Veridion

Veridion tracks weekly changes across more than 134 million companies in 250+ countries. It captures over 300 attributes per company, including product-level data, supplier and customer networks, and commercial footprint signals.

The service delivers that data through APIs and batch enrichment.

A SaaS company’s CI or market intelligence function can then plug structured signals directly into the systems they already use, whether that is a CRM, BI stack, or internal data lake.

That structure matters for competitive intelligence in particular. When competitor and supplier intelligence sits in the same data layer, you can join signals across them.

A hiring spike in a new region, combined with a supplier change, becomes one connected signal rather than two separate alerts.

For SaaS teams investing in CI capabilities, Veridion’s data for market intelligence and data for third-party risk management are particularly relevant.

Both are built to detect competitive and supplier-side threats earlier in the cycle.

Competitive intelligence used to be a document that an analyst owned and updated when a sales team complained loudly enough.

In a market where acquisition costs keep rising, and the average SaaS deal involves multiple competing evaluations, that approach no longer holds.

The companies that treat CI as a must, folded into product, pricing, retention, and threat planning, build an advantage that gives an edge.

The ones that do not keep discovering what the market decides after the decision has already been made.