Blog

Financial Data Enrichment Explained: What it is and Why it Matters

By: Stefan Gergely -

16 June 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

Key Takeaways:

Financial institutions and enterprises rely on data to make decisions every day. That data powers everything from customer onboarding to fraud detection and compliance reviews.

Yet a transaction record or customer profile rarely tells the full story.

A payment may be linked to a company you’ve never seen before. A vendor record may contain little more than a name and an address.

This is where financial data enrichment comes in. It adds valuable context to financial records, helping you understand the people and businesses behind the data.

Below, we’ll explain what financial data enrichment is, why it matters, and how to use it effectively.

Financial data enrichment is the process of adding relevant information to financial records to create a more complete picture of a customer or business.

Most financial records contain basic details such as account activity, transaction dates, and credit history. That information is useful, but it doesn’t always provide enough context.

Data enrichment supplements these traditional financial records with additional data to fill in gaps.

This data could include:

Many lenders, for example, already use this data enrichment to improve their understanding of customers.

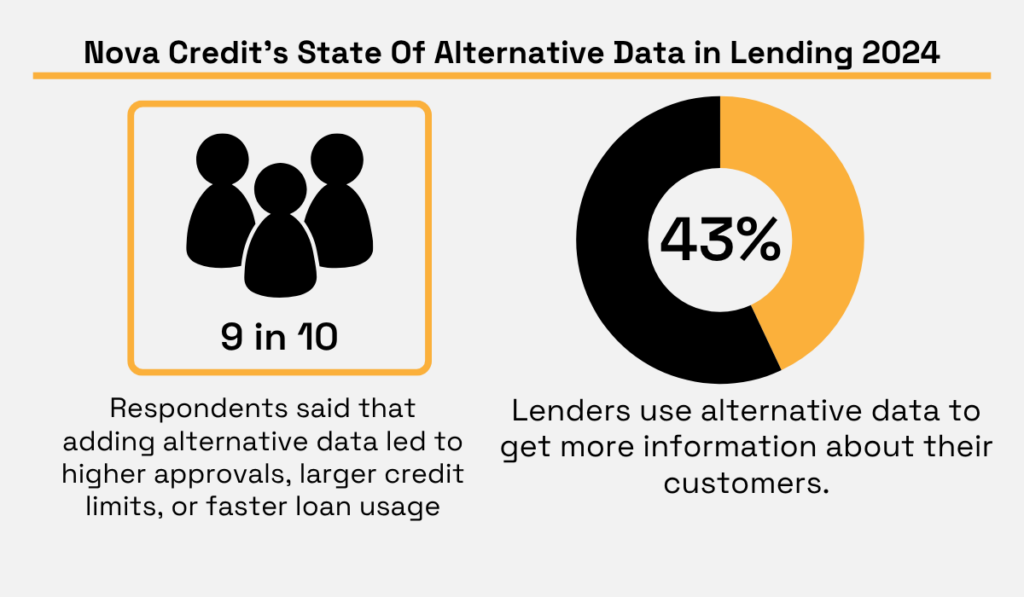

Nova Credit surveyed 125 decision-makers across banks, credit unions, fintechs, and other lending institutions in 2024.

The study found that 43% of lenders use alternative data to get more information about their customers.

And as a result, more than nine in ten respondents said that adding alternative data led to higher approvals, larger credit limits, or faster loan usage.

Illustration: Veridion / Data: Nova Credit

The value of financial data enrichment becomes even clearer when traditional financial records are incomplete.

Consider Fundfina, an Indian fintech that provides loans to micro and small enterprises.

The company estimates that about 80% of its customers have no formal credit history. That makes it difficult to evaluate borrowers using conventional underwriting methods alone.

To address this challenge, Fundfina combines credit information with alternative data such as business characteristics, partner information, and transaction records.

An analysis by CGAP found that enriched transactional data was just as effective as credit history when predicting repayment behavior.

The strongest results came from combining both sources, which improved prediction accuracy beyond either dataset on its own.

In short, financial data becomes more valuable when it’s supported by additional context.

That context comes from data enrichment, unlocking data-driven, better-informed decision-making across the board.

But what does this better decision-making actually look like?

Let’s explore some of the practical benefits of financial data enrichment.

If you’re a lender, bank, insurer, or fintech, you already collect large amounts of customer data, such as:

Those records show what your customers are doing, but they don’t always explain what they may need next.

Financial data enrichment fills those gaps by combining traditional financial records with additional information such as income, employment, and transaction data.

That level of detail matters because customers increasingly expect financial services to feel more personal.

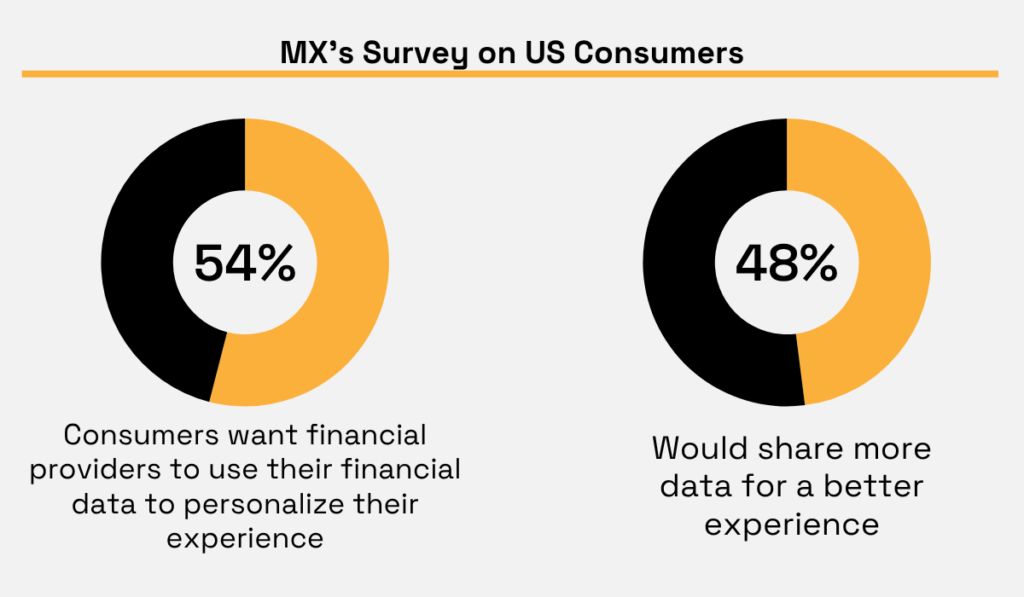

According to MX’s survey of more than 1,000 U.S. consumers, 54% want financial providers to use their financial data to personalize their experience.

Nearly half of respondents (48%) said they would share even more data if it led to a better experience.

Illustration: Veridion / Data: MX

In other words, customers increasingly expect personalized financial experiences. And many institutions are already using enriched data to do exactly that.

A LexisNexis Risk Solutions survey found that nearly all financial institutions using alternative data reported improvements in customer experience.

Nearly all respondents also said alternative data contributed to at least 15% revenue growth.

That’s because, simply put, better customer insights often lead to better customer experiences.

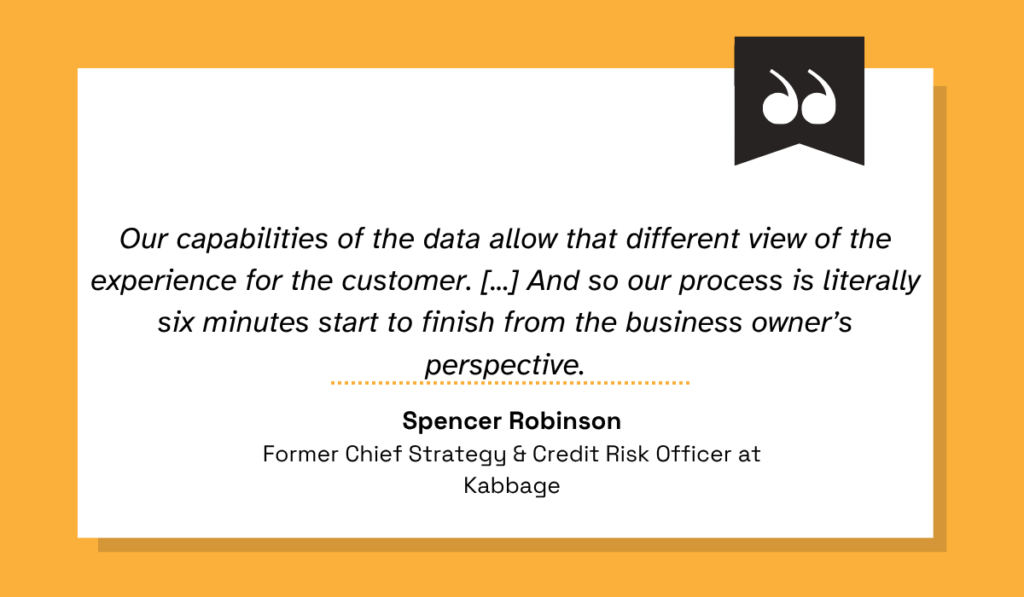

A good example of this is from Kabbage, a fintech lender later acquired by American Express.

Traditional lenders often rely on documents such as tax returns, financial statements, and credit scores to evaluate small businesses.

However, Kabbage expanded that view by also using live data from sources such as PayPal transactions, eBay sales, shipping records, and QuickBooks accounts.

This helped Kabbage make lending decisions in as little as six minutes.

For small business owners, that meant getting answers in minutes rather than waiting weeks for a traditional lender to review an application.

Spencer Robinson, head of strategy for the company, commented:

Illustration: Veridion / Quote: Knowledge at Wharton Podcast

This shows you can better understand your customers and deliver more relevant experiences by looking beyond basic financial records.

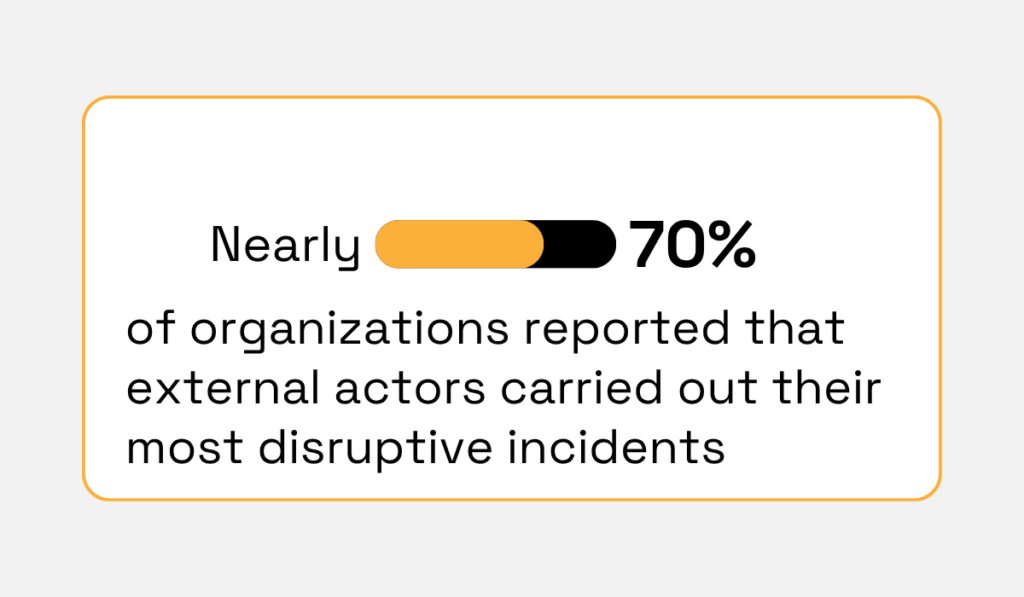

Your internal systems tell you what happened inside your organization, but it’s hard to verify whether a payment is being sent to the right person or whether a business is legitimate

That matters because many fraud threats originate outside your organization.

According to PwC’s Global Economic Crime and Fraud Survey, nearly 70% of organizations that experienced fraud said external actors carried out their most disruptive incidents.

Illustration: Veridion / Data: PWC

To identify those threats, you often need information that does not exist in your internal records.

Financial data enrichment fills that gap by connecting transactions to additional data such as account ownership, business identity, and other verification records.

The UK’s Confirmation of Payee (CoP) system is a great example of how effective data is in combating fraud.

For years, organizations were frequent targets of corporate invoice fraud.

Criminals would alter payment details on invoices and redirect funds to their own accounts. And because banks could only verify that an account existed, many fraudulent payments appeared legitimate.

The UK Payment Systems Regulator introduced Confirmation of Payee to address the problem.

It’s a system that allows banks to exchange account ownership data in real-time.

So before a payment is sent, banks now check whether the account holder’s legal name matches the name provided by the sender.

That extra layer of verification helps organizations spot suspicious payments before funds leave their accounts.

Kate Fitzgerald, Head of Policy at the PSR, the UK’s statutory economic regulator for payment systems, praised the tool:

“Confirmation of Payee has quickly become an essential anti-fraud tool. Since its launch in 2020, more than 2.5 billion checks have been completed […] ensuring widespread checks and safeguards, implementing strong reputational and financial incentives for industry action, and promoting better data and intelligence sharing.”

The main takeaway is clear: when you combine internal payment data with external verification data, you can identify fraud risks that would otherwise remain hidden.

Compliance teams are expected to identify suspicious activity, screen customers against sanctions lists, and monitor transactions for signs of financial crime.

But when monitoring and screening systems operate with incomplete information, compliance failures become more likely.

The consequences of this can be expensive.

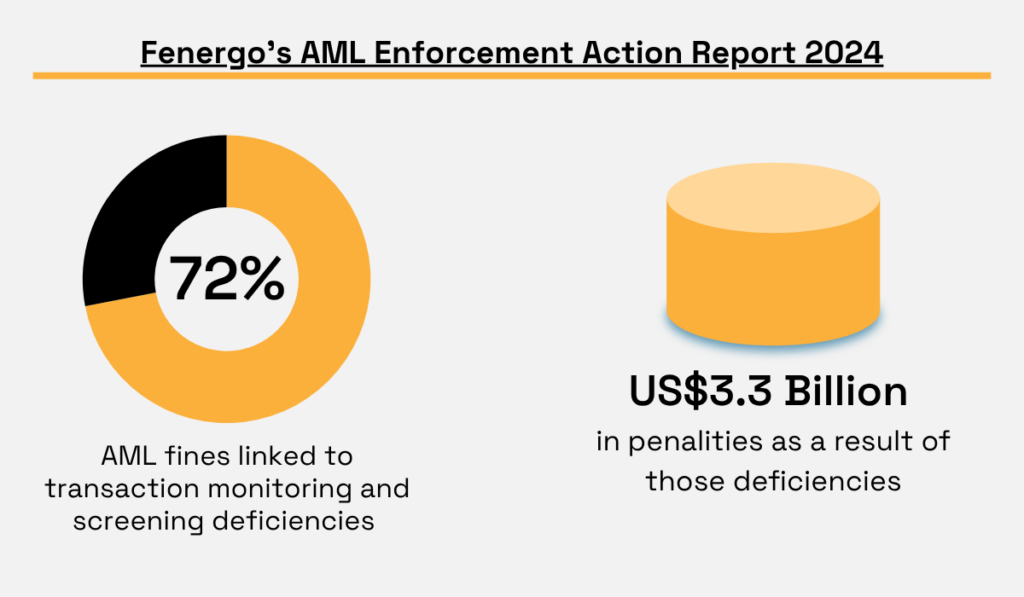

According to Fenergo’s AML Enforcement Action Report 2024, deficiencies in transaction monitoring and screening systems accounted for 72% of all global AML fines issued during the year.

Those failures resulted in more than $3.3 billion in regulatory penalties.

Illustration: Veridion / Data: Fenergo

In the end, screening systems can only identify risks when they have access to complete and current information.

That is where financial data enrichment comes in, continuously updating customer, ownership, sanctions, and transaction records.

This gives compliance teams a more reliable foundation for monitoring and screening activities.

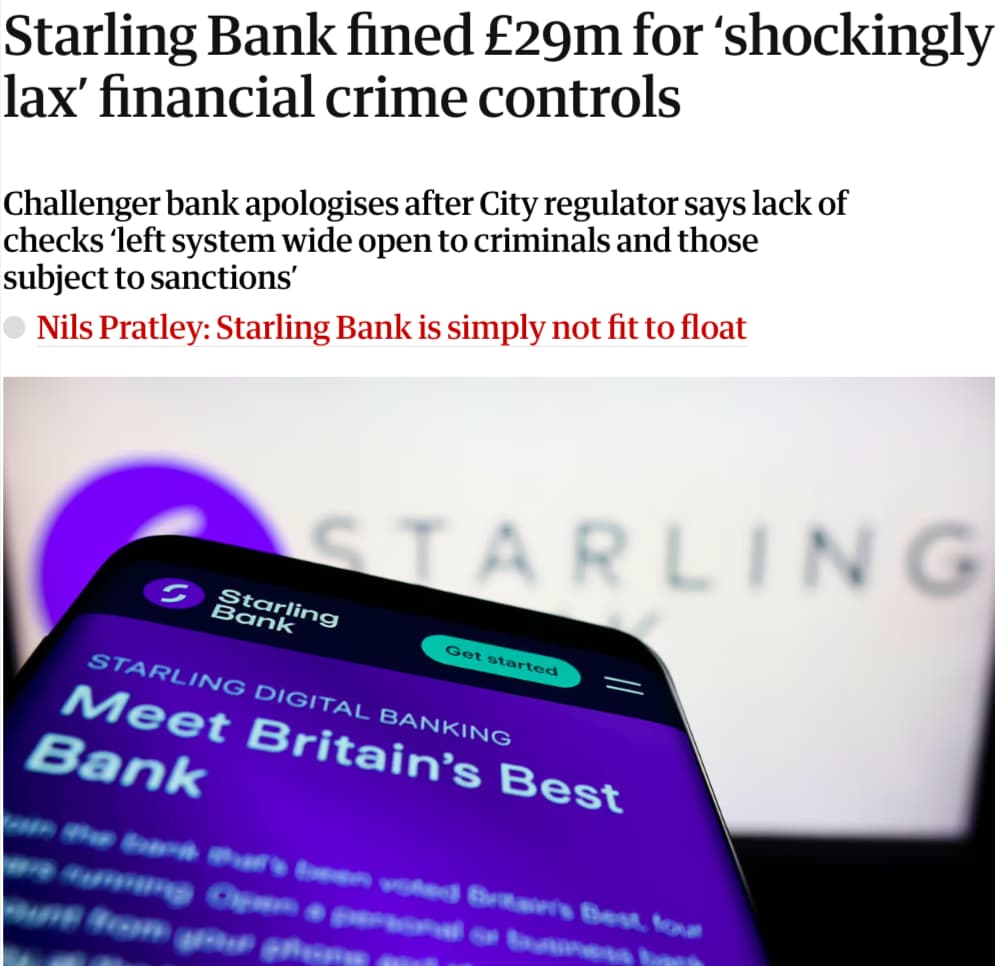

You can see the cost of missing information in the case of Starling Bank, a UK digital bank that grew from roughly 43,000 customers in 2017 to 3.6 million by 2023.

In 2024, the FCA fined Starling £29 million after identifying serious weaknesses in its financial crime controls.

Source: The Guardian

An internal review found that the bank’s automated screening system had been checking customers against only a fraction of the full sanctions list since 2017.

As a result, Starling opened more than 54,000 accounts for high-risk customers between 2021 and 2023 despite regulatory restrictions designed to prevent exactly that outcome.

The bank had screening technology in place. But the problem was that the system was working with incomplete sanctions data.

Financial data enrichment keeps information current, helping you identify compliance risks earlier and reduce the likelihood of costly regulatory failures.

Financial data enrichment works best when it’s built on accurate and well-managed data.

That starts with making sure your existing records are clean and reliable.

Financial data enrichment can’t fix existing data problems.

When your customer records contain duplicates, missing information, or inconsistent formatting, those issues carry over into the enriched dataset.

You’ll end up with more data, but not necessarily better insights.

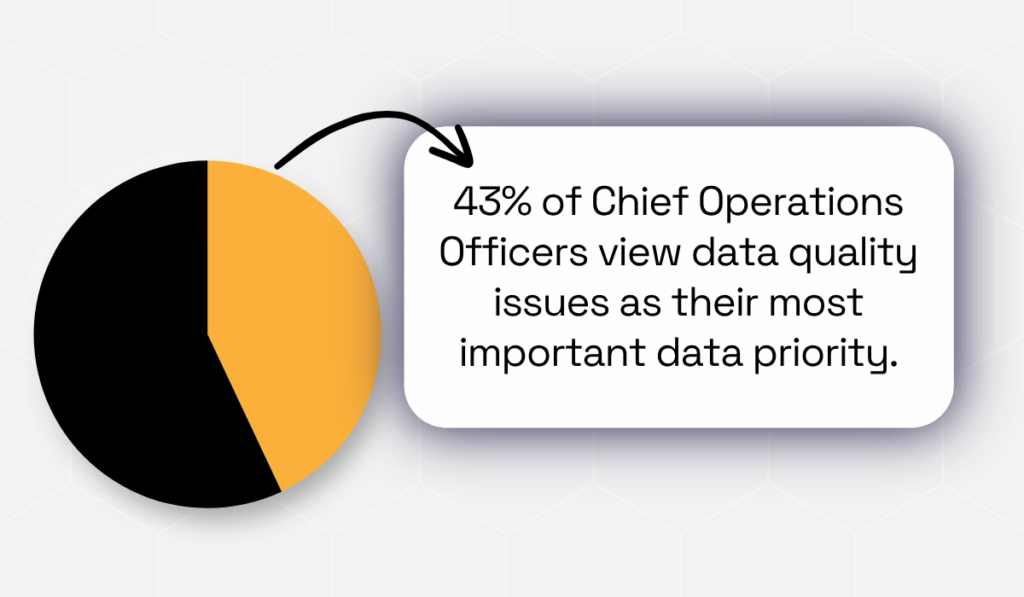

That’s why research shows that data quality remains a major concern for business leaders.

A 2025 IBM Institute for Business Value report found that 43% of Chief Operations Officers view data quality issues as their most important data priority.

Illustration: Veridion / Data: IBM

The financial impact is substantial, too.

According to Forrester’s Data Culture and Literacy Survey, more than one-quarter of data and analytics professionals who cite poor data quality as a barrier estimate it costs their organizations over $5 million annually.

Seven percent put those losses at more than $25 million annually.

Financial data enrichment, unfortunately, is tripped up by such inefficiencies, too.

If a customer appears multiple times in your systems under slightly different names, enrichment tools may struggle to build a complete profile.

Saga, a UK company offering insurance, travel, and financial products to older consumers, encountered exactly this problem.

Customer information was spread across multiple databases and applications. Duplicate records made it harder to build a complete view of customers.

This increased the risk of poor communication, missed sales opportunities, and weaker fraud detection.

To address the issue, Saga launched a data quality initiative to improve governance and reduce duplicate records.

The company cut duplicate customer records from roughly 5% of its database to less than 1%, eliminating tens of thousands of duplicates.

Source: Experian

The impact was immediate.

Saga improved audience targeting, delivered more relevant communications, and saved approximately £300,000 in direct marketing costs.

Saga’s experience shows the value of improving data quality before trying to generate new insights from customer data.

This cleaning exercise increases matching accuracy and reduces the likelihood of generating incomplete or misleading insights.

So before enriching your financial data:

Because financial data enrichment delivers better results when the underlying data is already accurate and consistent.

Financial data enrichment gives you access to more information. But this also means more responsibility.

As you collect more data, the potential cost of a breach grows as well.

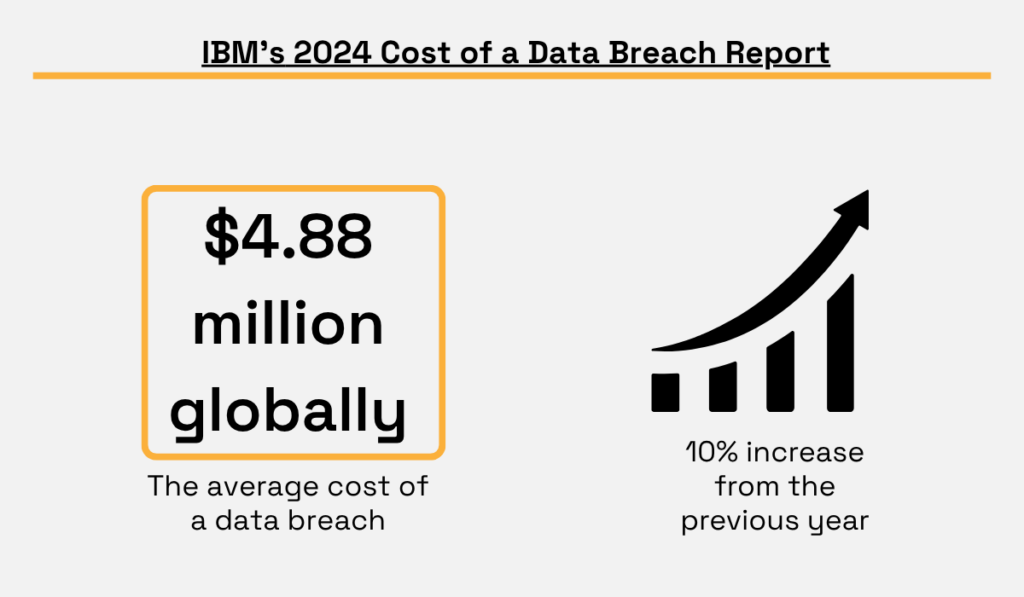

In fact, IBM’s 2024 Cost of a Data Breach Report found that the average cost of a data breach reached $4.88 million globally.

That’s a 10% increase from the previous year and the largest annual jump since the pandemic.

Illustration: Veridion / Data: IBM

The disruption can last even longer than the financial impact.

According to the same report, 70% of organizations experienced significant business disruption after a breach.

Among the small percentage of organizations that fully recovered, most needed more than 100 days to do so.

Capital One, one of the largest banks in the United States, offers a clear example of what can happen when sensitive financial data is not adequately protected.

In 2019, an attacker exploited a misconfigured firewall in the bank’s cloud infrastructure and gained access to personal information belonging to more than 100 million individuals across the United States and Canada.

The exposed data included names, addresses, dates of birth, self-reported income information, credit-related data, and portions of transaction records.

The consequences were substantial.

In 2020, the Office of the Comptroller of the Currency fined Capital One $80 million for deficiencies in its risk management and security controls. The company later agreed to pay $190 million to settle customer lawsuits related to the breach.

Source: Reuters

Capital One had access to enormous amounts of customer and financial data. The problem was that a security gap allowed an attacker to access that data.

This is why the value of enriched financial data depends on your ability to protect it.

So before working with a financial data enrichment provider, ask:

You should also review the provider’s privacy policy to understand how customer data is collected, stored, and protected.

Here’s an example of what that might look like:

Source: Veridion

Strong privacy and security practices help ensure that the insights you get do not come at the expense of customer trust or regulatory compliance.

Financial data becomes more valuable when you combine it with business context.

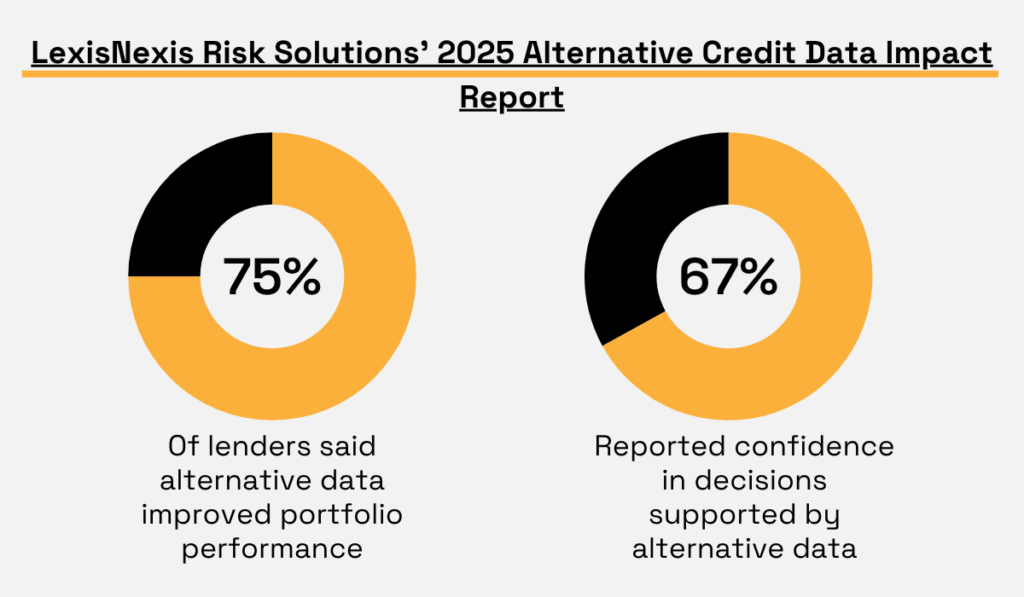

According to LexisNexis Risk Solutions’ 2025 Alternative Credit Data Impact Report, 75% of lenders said alternative data improved portfolio performance, while 67% reported greater confidence in decisions supported by alternative data.

Illustration: Veridion / Data: LexisNexis

Respondents also reported using alternative data across acquisition, underwriting, account management, and collections to identify risk earlier and make more informed decisions throughout the credit lifecycle.

Organizations use external data because it provides context that financial records alone can’t.

Internal data shows you what has happened. External data helps explain why it happened and what might happen next.

Veridion, a business intelligence platform powered by AI, can help.

It builds detailed profiles of businesses by continuously collecting and structuring information from company websites, public records, social media profiles, press releases, and other sources.

The result is a database covering more than 130 million businesses worldwide, with information refreshed regularly to reflect changes in how companies operate.

Its Match & Enrich API can also supplement existing records, refresh outdated information, reduce data gaps, and help build more complete business profiles without relying on manual research.

You can learn more in the video below:

Source: Veridion on YouTube

So when choosing an enrichment provider, look for one that offers broad coverage, frequent data refreshes, and APIs that fit your existing systems.

The more complete your view of a customer or business, the more value you can unlock from your data.

Your internal records already contain valuable information. External data adds the context needed to understand customers, assess risk, and spot opportunities more clearly.

The results can be significant. Better customer insights. Stronger fraud detection. More effective compliance programs.

The challenge is that business information rarely stays the same.

Companies grow, markets shift, and risks evolve. Financial data enrichment helps ensure the information you rely on keeps pace with those changes.