Blog

How to Assess Your Vendor Concentration Risk

By: Auras Tanase -

27 March 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

Key Takeaways:

Your largest supplier misses a shipment. At first, everything seems manageable.

But then, you realize two of your “backup” vendors operate in the same industrial zone.

A third vendor relies on the same upstream component manufacturer.

So, qualification timelines for alternatives stretch into months. Within weeks, production stalls.

This is how vendor concentration risk unfolds.

Not as a single failure, but as a network of hidden dependencies exposed at the worst possible time.

Managing vendor concentration risk requires more than awareness.

It demands structured analysis, clear visibility, and deliberate diversification.

This article outlines a practical, step-by-step framework for identifying exposure, uncovering hidden dependencies, and building resilient vendor alternatives before disruption forces your hand.

When a single supplier accounts for a disproportionate share of spend, it introduces structural concentration risk that can quickly translate into operational instability during disruptions.

Real-life examples show just how serious this can be.

During the automotive semiconductor shortage in 2020-2022, major automakers such as Ford and General Motors experienced production slowdowns due to their heavy reliance on a limited number of semiconductor vendors.

Source: CNBC

The crisis illustrated how upstream dependency, even within a diversified supplier base, can trigger outsized operational disruption.

But vendor concentration risk is not limited to manufacturing.

Reliance on key third-party providers for security, software, logistics, or data can create systemic vulnerabilities across the enterprise.

Rob Demain, CEO & Founder of e2e-assure, an end-to-end third-party risk management platform, underscores this:

Illustration: Veridion / Quote: IT Pro

He urges leaders to move beyond surface-level vendor oversight and assess concentration risk more holistically.

The foundation of any concentration risk assessment is identifying which vendors are truly critical to your business.

Start with objective indicators like total spend and transaction volume.

For instance, calculating the percentage of total annual procurement spend attributed to the top three or five suppliers is a common method for identifying high concentration risk.

Figures exceeding 60% for the top three vendors signal an elevated risk profile.

This is a useful benchmark for early assessment, but it only tells part of the story.

A vendor’s real importance often lies in how deeply embedded it is in your operations.

To get an accurate picture, look beyond headline spend figures and examine which vendors support mission-critical products, services, or processes.

Ask questions such as:

Vendors that underpin core manufacturing steps, proprietary technology, regulatory compliance, or customer-facing services often carry disproportionate risk, regardless of what you pay them.

Low-spend vendors can still pose a high-concentration risk.

A niche supplier providing a specialized component, a single-source data provider, or a vendor supporting a critical IT or logistics function may have an outsized operational impact.

Identifying these dependencies early ensures your risk assessment reflects operational reality, not just procurement totals, and sets a solid foundation for deeper concentration analysis.

The next step is evaluating whether your vendors are financially or operationally capable of sustaining your organization’s reliance on them.

When a supplier accounts for a significant share of your spend or underpins a core function, its financial health becomes a direct risk to your business.

Supplier viability is a measurable risk.

Sphera’s 2026 Supply Chain Risk Report highlights that supplier viability, which includes financial and operational stress, remains the largest category of supplier risk events, increasing about 10% in 2025 compared to 2024.

Additionally, 73% of organizations reported financial or operational losses due to supply chain disruptions in the past 12 months, with an average of more than three material disruptions per organization.

Illustration: Veridion / Data: Sphera

This directly links supplier financial stress to operational loss and disruption, not just theoretical risk.

Corey Rhodes, CEO of Everstream Analytics, emphasizes this:

Illustration: Veridion / Quote: Forbes

Operational capacity matters just as much as financial strength.

Simply put, vendors must also have the operational capacity to deliver reliably.

So, assess whether they have sufficient production capacity, geographic redundancy, inventory buffers, and workforce stability to meet demand.

This will be particularly relevant during peak periods or market shocks.

Limited production capacity or single-site operations can become bottlenecks, even if alternative vendors are available.

When analyzing financially critical vendors, assess the following:

| Factor | Key Question to Ask |

|---|---|

| Revenue and margin trends | Are the vendor’s revenues and profits stable, growing, or declining? Could downward trends signal financial stress? |

| Debt levels and liquidity | Does the vendor have sufficient cash flow and manageable debt to fund operations, scale if needed, or survive market shocks? |

| Credit ratings or risk scores | How do independent credit agencies or risk scores rate this vendor? Do these ratings indicate high default or insolvency risk? |

| Customer concentration | Would your business account for a material portion of their revenue? Could losing your account destabilize them? |

A vendor that is highly concentrated in your supply base and financially fragile poses a compounding risk exposure.

Concentration risk isn’t just about how much you spend.

It’s also about how much you depend on a vendor, and whether they can withstand stress.

Analyzing financial stability and operational resilience ensures your organization relies on vendors that can scale, adapt, and sustain performance during disruptions.

Without this step, even a well-diversified vendor portfolio can conceal hidden fragility.

Next, you want to understand where your critical vendors operate and the external risks that could affect them.

Geographic risk exposure can create vulnerabilities even when a vendor is financially strong and operationally capable.

A McKinsey study across global value chains found that, for 180 traded products, one country accounts for 70% or more of exports, creating potential supply bottlenecks if that region experiences a shock.

External factors to consider include:

| Natural Disasters | Floods, earthquakes, hurricanes, or wildfires can disrupt operations unexpectedly. |

| Geopolitical Instability | Civil unrest, trade restrictions, sanctions, or military conflicts can hinder vendor performance. |

| Regulatory Changes | Sudden changes in local laws, tariffs, or export controls can affect supply. |

| Infrastructure Dependencies | Reliance on shared utilities, transport networks, or communication hubs can magnify operational risk. |

Let’s illustrate this with an example.

In late September 2024, Hurricane Helene caused significant damage to the Baxter manufacturing facility in Marion, North Carolina.

Source: Baxter

The hurricane disrupted Baxter’s manufacturing capacity for IV fluids and other critical medical supplies.

While production has since resumed, the event highlights how a single regional disruption can ripple across critical supply chains and affect downstream operations.

Arpana Amin, Global Head of Supply Chain Finance at HSBC, underscores the importance of geographic risk awareness:

Illustration: Veridion / Quote: Treasury Today

Concentration risk often arises when multiple critical vendors are clustered in the same region or share infrastructure.

For example, several suppliers of a specialized component located in the same industrial zone or dependent on a single port can create a single point of failure.

Even with multiple vendors, geographic clustering can leave organizations exposed to localized shocks.

So, mitigating geographic risk requires thoughtful diversification.

Spread critical vendors across regions, countries, and infrastructure networks to reduce vulnerability to natural disasters, geopolitical events, and infrastructure failures.

Geographic diversification is as important as supplier diversification in ensuring resilient, reliable supply chains.

The next layer of vendor concentration risk analysis is mapping how each critical vendor supports your organization across products, business units, and regions.

Because unfortunately, concentration risk doesn’t only arise from spend or geography.

It often emerges from structural dependencies embedded within workflows, systems, and revenue streams.

Sure, a vendor may appear diversified at first glance, serving multiple departments or operating in several regions.

However, deeper analysis often reveals that the same vendor underpins:

When a vendor supports multiple operational layers, disruption doesn’t remain contained.

It cascades across departments, customer segments, and regional operations simultaneously.

Without structured dependency mapping, organizations often underestimate their exposure.

For example, a cloud provider may support marketing analytics, customer-facing applications, and internal reporting systems.

Similarly, a logistics partner may serve multiple brands within the same corporate group, and a niche component supplier may feed into several high-margin product lines.

On paper, these relationships may appear isolated.

In practice, they form an interconnected web of reliance.

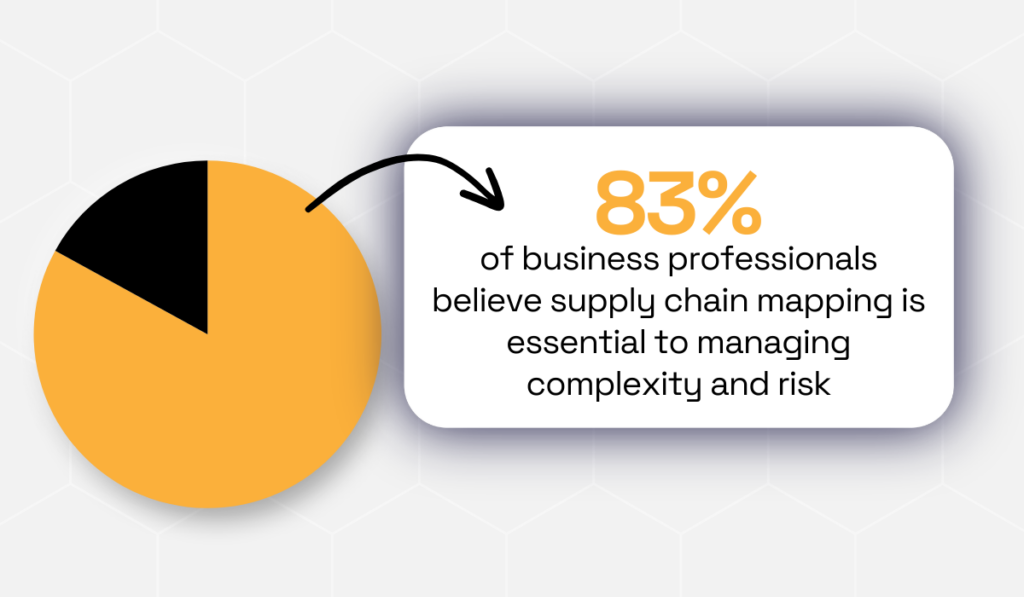

According to a poll by B2BE, 83% of business professionals believe supply chain mapping is essential to managing complexity and risk.

Illustration: Veridion / Data: B2BE

Yet, manually identifying hidden overlaps across vendors, locations, and business functions can be extremely complex, especially for large enterprises with thousands of suppliers.

This is where enriched supplier intelligence becomes critical.

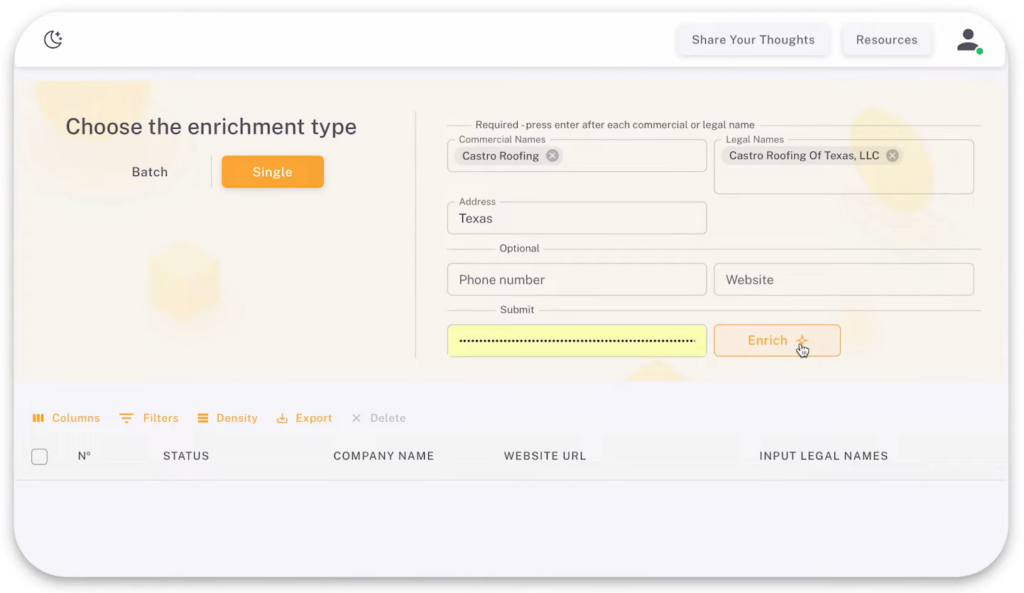

Veridion’s Match & Enrich API transforms minimal vendor information into comprehensive risk intelligence.

Source: Veridion

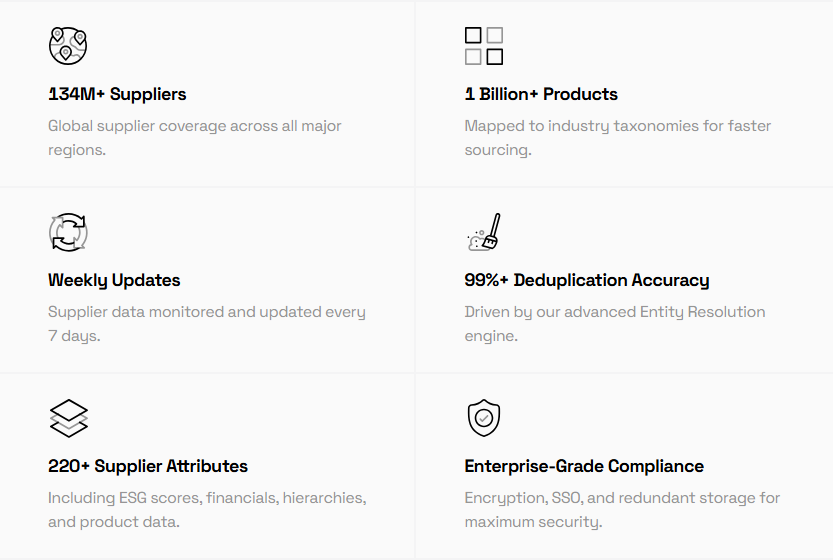

By submitting only a company name and location, the API matches the input against 134+ million companies and returns enriched profiles with over 220 data attributes, including industry classifications, financial estimates, locations, and operational details.

Source: Veridion

How does this work for concentration risk assessment?

The API creates a “golden record” for each vendor by cleaning, de-duplicating, and standardizing data across ERPs and procurement systems with weekly updates.

This enriched data enables multi-dimensional concentration risk analysis, including:

Source: Veridion

By combining internal procurement data with enriched external intelligence, you can gain visibility into how deeply vendors are embedded within workflows and revenue streams, and where structural concentration risk truly exists.

Because you can’t manage what you can’t see.

Now, it’s time to assess how easily each vendor could be replaced in the event of disruption.

On paper, many organizations appear to have alternative suppliers available.

In practice, substitutability is often far more complex.

Replacing vendors often requires navigating:

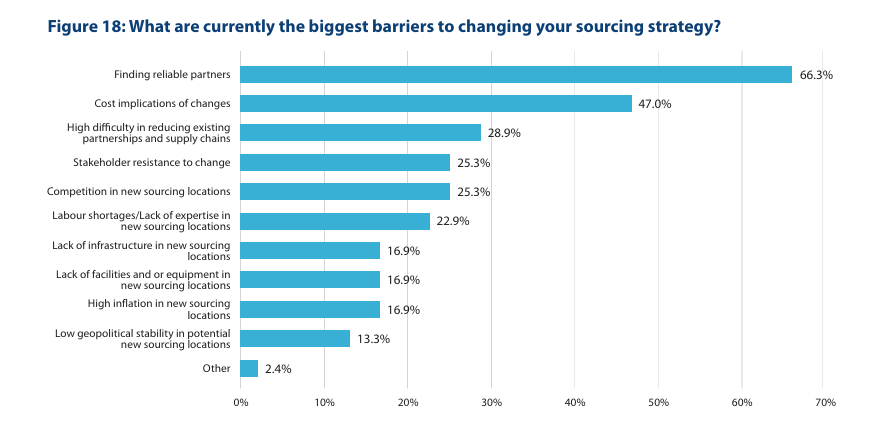

According to a Reuters Events Supply Chain white paper, 66.3% of organizations cite difficulty finding reliable alternative partners as the biggest barrier to changing sourcing strategies, while 47% point to cost implications as a major hurdle.

Source: WITA

These aren’t minor obstacles.

They reflect long onboarding cycles, certification requirements, system integrations, and relationship-specific investments that make switching slow, expensive, and operationally disruptive.

A supplier with specialized capabilities, proprietary technology, or lengthy qualification processes can create de facto concentration risk, even if it represents only a moderate share of spend.

In such cases, theoretical supplier diversification doesn’t equal practical replaceability.

Ask the following questions to evaluate vendor substitutability:

Ultimately, concentration risk isn’t defined by how many suppliers you list in your system.

It’s defined by how quickly and smoothly you can replace them when disruption occurs.

Evaluating substitutability ensures your vendor diversification strategy is actionable rather than theoretical.

The final step involves proactive contingency planning.

Identifying critical vendors and evaluating their risk profiles is only valuable if your organization also understands the viable alternatives.

This step requires proactively identifying backup or replacement vendors for highly concentrated suppliers before disruption occurs.

Waiting until a disruption unfolds significantly reduces negotiating power, increases onboarding delays, and amplifies operational risk.

For each high-risk or highly concentrated vendor, you should:

Organizations are increasingly building supplier alternatives to improve resilience.

According to the McKinsey Supply Chain Risk Survey, 73% of business leaders reported progress on dual-sourcing strategies, indicating growing recognition of pre-qualified alternatives.

Illustration: Veridion / Data: McKinsey

Pre-qualification is important because switching vendors can take months, especially in highly regulated industries.

So, by assessing and documenting alternative vendors in advance, organizations can reduce response times and avoid scrambling under pressure.

For example, let’s assume you identify two potential alternative suppliers but don’t formally evaluate or qualify them.

When your primary vendor experiences production delays due to equipment failure, you discover that one alternative lacks sufficient production capacity and the other requires a six-month validation process.

Since you didn’t prequalify your alternatives, you must halt production for 8 weeks, resulting in delayed shipments and lost revenue.

Had you assessed and pre-qualified alternatives earlier, the switching timelines could’ve been significantly reduced.

Identifying alternatives strengthens both short-term response capability and long-term resilience.

A case in point is Barilla, a top Italian pasta maker.

Source: Procurement Leaders

Under the leadership of VP of Purchasing Luigi Ganazzoli, Barilla addressed inflation by expanding its supplier base for key inputs, including packaging and ingredients, and qualifying board suppliers from the Far East in response to European scarcity.

They also pushed technical teams to adjust certain ingredient specifications to enable sourcing from additional suppliers, reducing reliance on a single source.

The takeaway?

Knowing vulnerabilities isn’t enough.

Vendor concentration risk is reduced only when credible fallback options are ready.

Pre-qualifying alternatives strengthens short-term response, enhances long-term resilience, and ensures disruption doesn’t translate into lost revenue.

Vendor concentration risk doesn’t fail loudly.

It happens suddenly and quietly.

By the time disruption occurs, the exposure has usually been embedded in your supply base for years.

Resilient organizations don’t wait for proof. They map dependencies, validate alternatives, and diversify before disruption forces their hand.

Remember, visibility and preparation determine resilience.

Act now before concentration risk becomes an operational reality.