Blog

What Are the Benefits of Insurance Data Enrichment?

By: Stefan Gergely -

25 February 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

Key Takeaways:

Your risk decisions are only as strong as the data behind them.

Fragmented, outdated, or incomplete data slows down underwriting, pricing, and claims decisions, creating blind spots that are difficult to detect until they escalate.

So, if you are looking to improve accuracy without adding complexity to your workflows, you are in the right place.

In this article, we will examine how insurance data enrichment addresses critical data gaps, enhances decision-making, and enables insurance teams to operate with greater speed, clarity, and certainty.

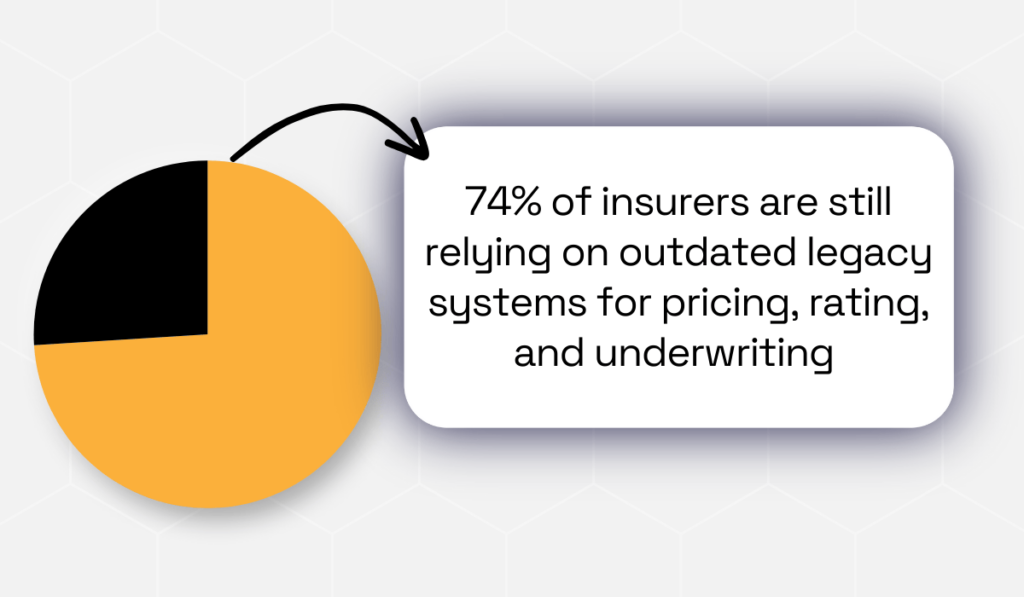

Traditional underwriting has some blind spots.

For instance, one industry study found that about 74% of insurers still use outdated legacy technology for pricing, rating, and underwriting tasks, which amplifies those blind spots.

Illustration: Veridion / Data: Earnix

Teams are often working with incomplete application forms, outdated classifications, and information that doesn’t reflect how a business actually operates today.

That is a problem when you’re trying to assess real risk.

Insurance data enrichment fixes this by filling in the gaps.

It layers in verified firmographic data, financial details, operational information, and ownership records.

Instead of making educated guesses, you get a complete picture of who you’re insuring and what their actual exposures are.

When it comes to your day-to-day work, this means you can see:

These are the signals that actually matter when you’re evaluating risk.

Why?

Because they help you:

Take location data as an example.

Historically, insurers treated location as a simple data point, but enriched location intelligence goes deeper, showing you that risk can vary, even on the same street.

Two properties might share an address range.

But one could sit near a high-traffic intersection with elevated crime exposure. The other might be in a low-speed zone near schools and well-maintained commercial areas.

Without enrichment, you’d never see that difference.

With it, you can price each policy based on real environmental context, not “good enough” averages.

Data enrichment also keeps your risk assessments current.

Let’s use auto insurance, for example.

With driving behavior data, you can price premiums based on how someone actually drives, not just their demographics.

Safe drivers get rewarded. High-risk behavior gets priced appropriately.

The same principle applies to commercial underwriting.

As a business changes new locations, different operations, and changing exposure levels, enriched data keeps your risk assessment aligned with reality.

For you, this accuracy translates directly into better loss prediction and healthier loss ratios.

In 2024, the US P&C industry’s combined ratio improved markedly.

The sector’s net combined ratio moved from 101.6% in 2023 to 96.5% in 2024, with loss-ratio improvements accounting for most of that gain.

It’s a reminder that better risk pricing reduces surprises at claim time.

When you price risk correctly from the start, you see fewer surprises at claim time.

For policyholders, it means fairer pricing based on their individual risk profile rather than broad, outdated classifications.

Enriched data replaces assumptions with evidence. That means smarter underwriting decisions, more competitive pricing, and stronger long-term portfolio performance.

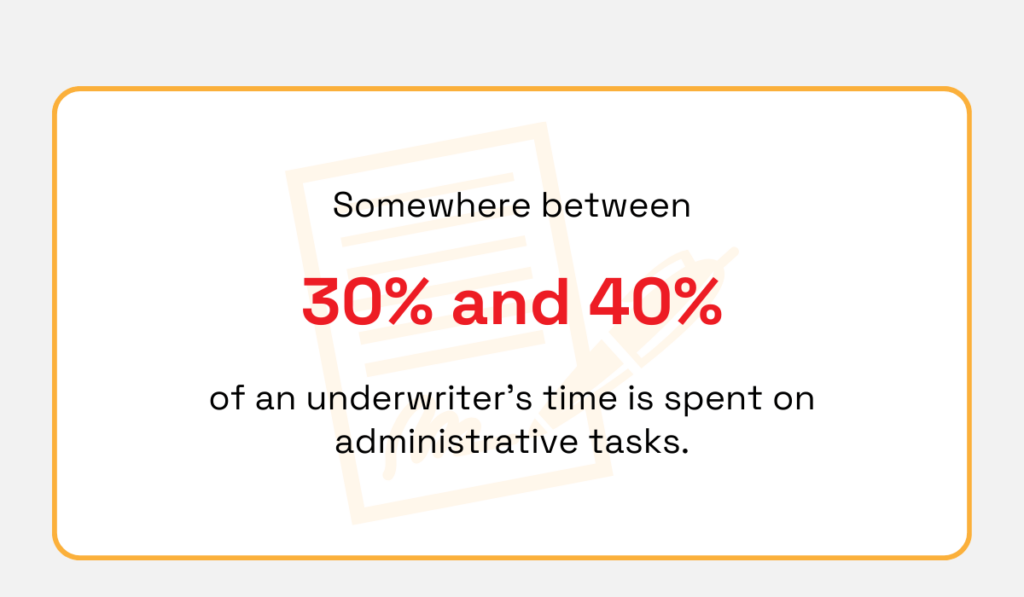

Data enrichment removes the slowest part of your process: manual data collection and verification.

McKinsey studies estimate that underwriters spend 30–40% of their time on administrative tasks, such as rekeying data or manually executing analyses.

Illustration: Veridion / Data: McKinsey

That’s the time that could’ve been spent on risk analysis or decision-making.

Think about how much time you spend searching for missing details, cross-checking records, or emailing applicants for clarification.

Enrichment automates all of that. The moment a submission hits your desk, the system pulls in external data automatically.

Even when an application only has basic inputs, like a company name or address, enrichment fills in the rest.

You get validated firmographic data, operational details, and risk-related information instantly without waiting or follow-up emails.

This automated pre-fill process shortens turnaround times without cutting corners.

Applications arrive already populated with consistent, verified information. You can jump straight into analysis instead of spending hours on preparation.

Enriched risk profiles also reduce back-and-forth with applicants. There’s less rework from data errors. Every submission you evaluate uses the same high-quality inputs.

The result is faster quotes, quicker binding, and fewer bottlenecks, all while maintaining the controls you need for accurate underwriting decisions.

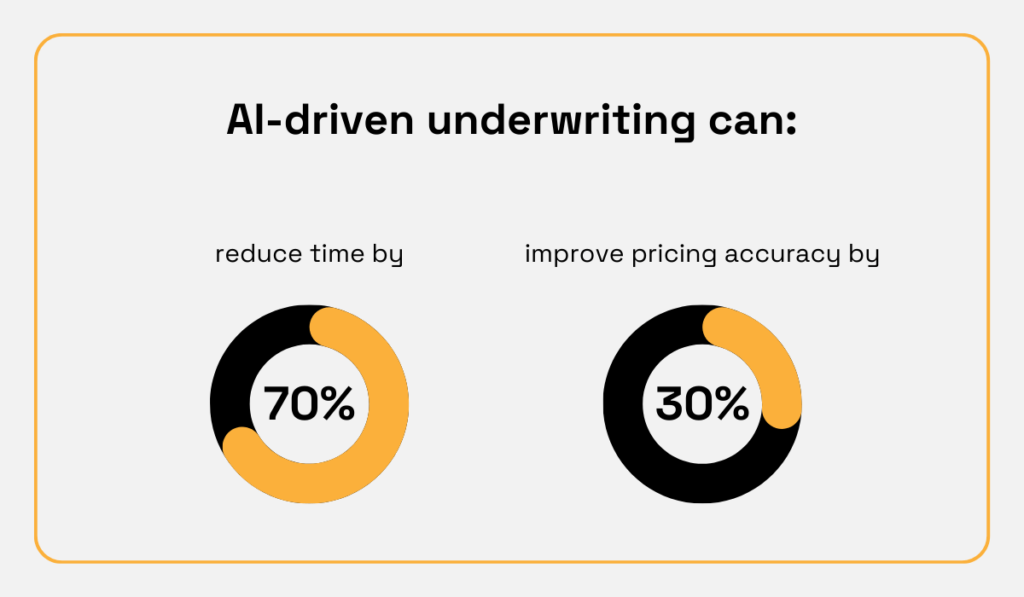

In fact, research from NTT Data shows that AI-driven underwriting can significantly save time and improve pricing accuracy, significantly reducing loss ratios.

Illustration: Veridion / Data: NTT Data

This becomes especially valuable during peak submission periods.

When you’re processing large volumes under pressure, enrichment allows you to scale without lowering standards.

It shifts your focus away from repetitive tasks like data extraction, cleansing, and validation. You spend more time on higher-value judgment work instead.

Routine, low-complexity risks can flow through straight-through processing or even touchless underwriting. The system gathers data, scores the risk, and generates a decision in seconds.

More complex or high-severity exposures still get your expertise. But you’re starting from a strong foundation with all relevant data already centralized and modeled, not from a blank page.

This means your team can handle far more submissions with the same resources, even as workloads grow more complex.

Ultimately, these faster decisions:

In short, data enrichment makes underwriting a scalable, high-velocity process without compromising accuracy or control.

Data enrichment removes much of the friction that makes underwriting feel slow and frustrating for customers.

When applications are enriched upfront, customers don’t have to answer repetitive questions.

They don’t have to re-submit the same information or hunt down supporting documents after the fact.

Key details get filled and validated automatically behind the scenes, so applicants can move through the process quickly and confidently.

What used to feel like an interrogation starts to feel like a guided, efficient workflow that respects their time.

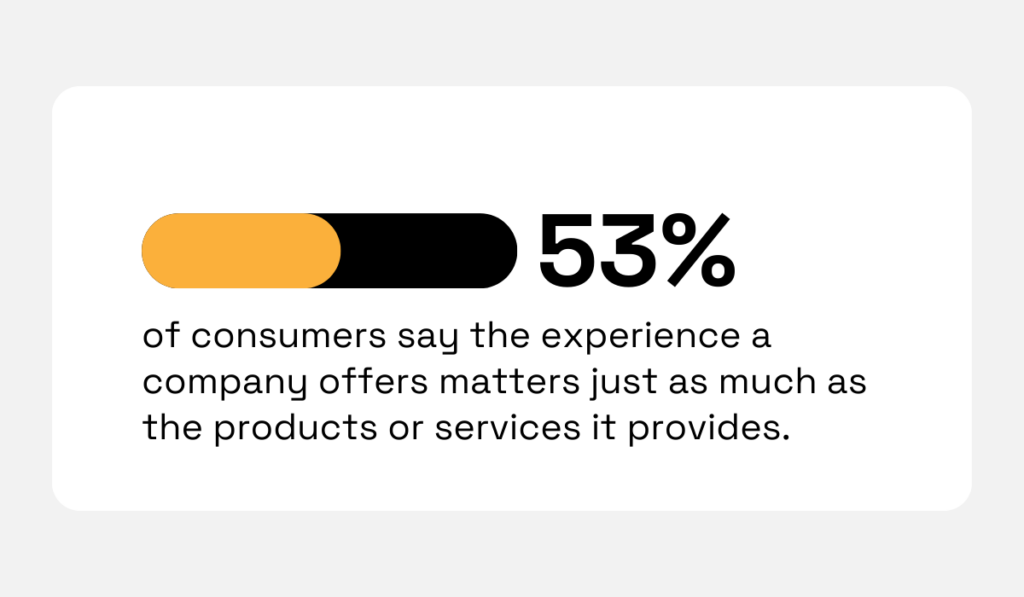

This is important because customers are judging brands by how easy and respectful the experience feels.

53% of consumers say the experience a company offers matters just as much as the products or services it provides.

Illustration: Veridion / Data: Forbes

This makes smooth underwriting a core part of your value proposition, not a mere operational detail.

When underwriting feels simple and intuitive, customers are far more likely to complete applications instead of abandoning them halfway through.

Because you’re working with complete, enriched risk profiles from the start, customers get faster decisions with far fewer follow-up requests.

Instead of waiting days for clarification emails or additional data calls, they see quotes, approvals, or adjustments much sooner.

You can already see this transformation happening in practice.

Brazilian life insurer MAG Mongeral Aegon recently implemented Munich Re Automation Solutions’ SARA risk assessment platform to streamline its new business underwriting.

Source: Insurance Business Mag

By integrating enriched data directly into its existing systems, SARA now processes over 90% of life insurance applications in under two minutes at the point of sale, delivering instant decisions without compromising risk quality.

Alberto Abalo, CEO of Munich Re Life and Health for Southern Europe and Latin America, explained:

“By leveraging SARA, MAG will not only streamline its processes but is also enhancing the customer experience at the point-of-sale.”

For MAG, the speed gains weren’t operational, they became a competitive experience advantage.

This speed and clarity make the entire journey feel more transparent. Customers know what’s happening, why it’s happening, and when they can expect an outcome.

That transparency builds trust, especially in an industry where customers often interact with you during stressful or high-stakes moments.

And trust isn’t emotional.

Instead, it directly determines whether customers choose to stay with you long-term.

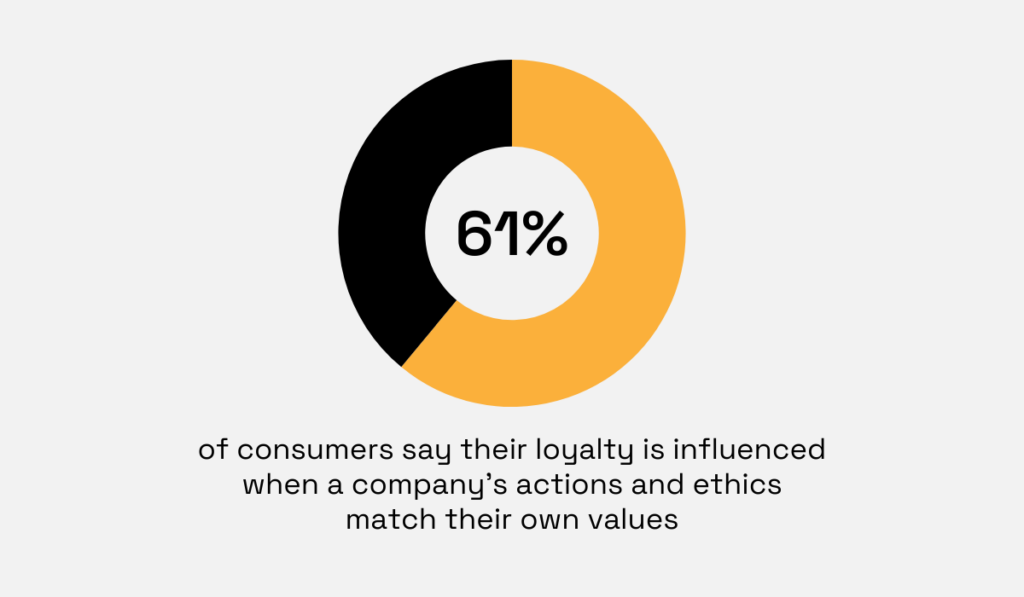

Research shows that 61% of consumers say their loyalty is influenced when a company’s actions and ethics align with their own values.

Illustration: Veridion / Data: Forbes

This makes transparency, fairness, and consistency in underwriting especially important.

When customers can see that decisions are data-backed, consistent, and respectful, they’re more likely to believe they’re being treated fairly.

Enrichment also lets you deliver more personalized experiences over time.

By connecting application data with historical policies, claims, interactions, and third-party signals, you build a 360-degree view of each customer.

This deeper understanding allows you to tailor coverage, communication, and even pricing to individual needs, instead of forcing everyone through the same rigid process.

That balance between digital efficiency and human reassurance is exactly what modern customers expect.

Stephen Rhee, global Chief Digital Officer at Gallagher, explained further:

Illustration: Veridion / Data: Insurance Business Mag

And when insurers get that balance right, the experience feels effortless.

Rhee adds:

“Companies that get the timing right create seamless experiences, merging digital convenience with personal service where it counts.”

When customers feel understood and properly served, their confidence in you grows along with the likelihood that they’ll stay.

In a market where switching providers is easier, experience is a major differentiator.

A smoother, faster, and more transparent underwriting journey reduces abandonment, improves satisfaction, and lowers churn.

Over time, those small improvements compound into stronger retention, higher lifetime value, and deeper customer loyalty built on trust.

Data enrichment makes inconsistencies much harder to hide.

When you are relying only on self-reported information, it’s easy for applicants to misstate facts, their location, operations, financials, and ownership structure.

Enriched data closes that gap by automatically cross-checking what applicants declare against multiple external sources.

Any mismatch becomes immediately visible. You get an early warning signal before coverage is bound.

These discrepancies often show up in subtle but meaningful ways.

A business might report operating in a low-risk industry. But registry data or web signals suggest higher-risk activities.

A declared address might not match official location records, and financial information might conflict with filings from trusted databases.

On their own, these differences might seem minor. But when enriched data brings them together in a single view, patterns of misrepresentation or potential fraud become much easier to spot.

This allows you to flag high-risk submissions early instead of discovering issues after losses occur.

Data intelligence platforms like Veridion amplify this capability significantly.

By aggregating and validating data from official registries, corporate filings, web signals, and other trusted sources, Veridion’s enrichment engine builds a unified, verified business profile.

Source: Veridion

It includes firmographics, operational footprints, industry classifications, and ownership structures.

Because each attribute is checked across multiple sources, omissions and inconsistencies stand out immediately.

Source: Veridion

For you, enriched data effectively becomes a built-in consistency check that runs automatically on every submission.

This kind of early fraud detection is especially important for protecting you from adverse selection and unnecessary financial losses.

When high-risk or misrepresented risks slip through underwriting, they lead to higher claims, distort portfolios, and damage profitability over time.

Enrichment helps prevent that by filtering out problematic submissions before they reach the policy stage.

Better data makes underwriting more accurate and safer. You are binding coverage based on verified reality, not incomplete or misleading information.

The gains from data enrichment compound when viewed across the insurer’s entire book.

By aggregating enriched attributes across all accounts, you gain solid portfolio analytics.

Patterns and concentrations that might go unnoticed at the policy level become clear.

And this visibility is no longer optional in today’s loss environment.

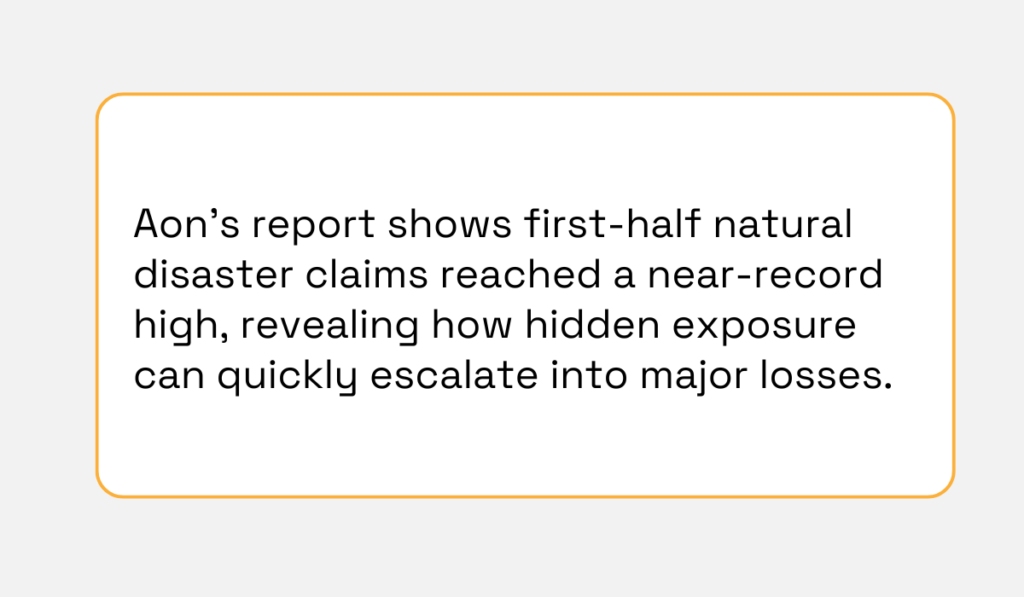

According to Aon’s 1H 2025 Global Catastrophe Recap, global natural disaster insurance claims were the second-highest on record for a first-half period.

Illustration: Veridion / Data: Aon

This underscores just how quickly unseen concentrations can turn into large-scale losses.

Without enriched portfolio data and modern modeling, insurers risk discovering these exposures only after losses have already materialized.

For example, enriched data might reveal that your book has an unintended concentration of clients in one disaster-prone ZIP code or too many policies in a single industry.

Recognizing these single points of failure early allows you to adjust underwriting guidelines, diversify risks, or purchase reinsurance strategically.

Beyond making each risk decision better, enriched data helps you evaluate the health of your entire portfolio.

You can model risk, assess current portfolios, and increase pricing accuracy for new policies.

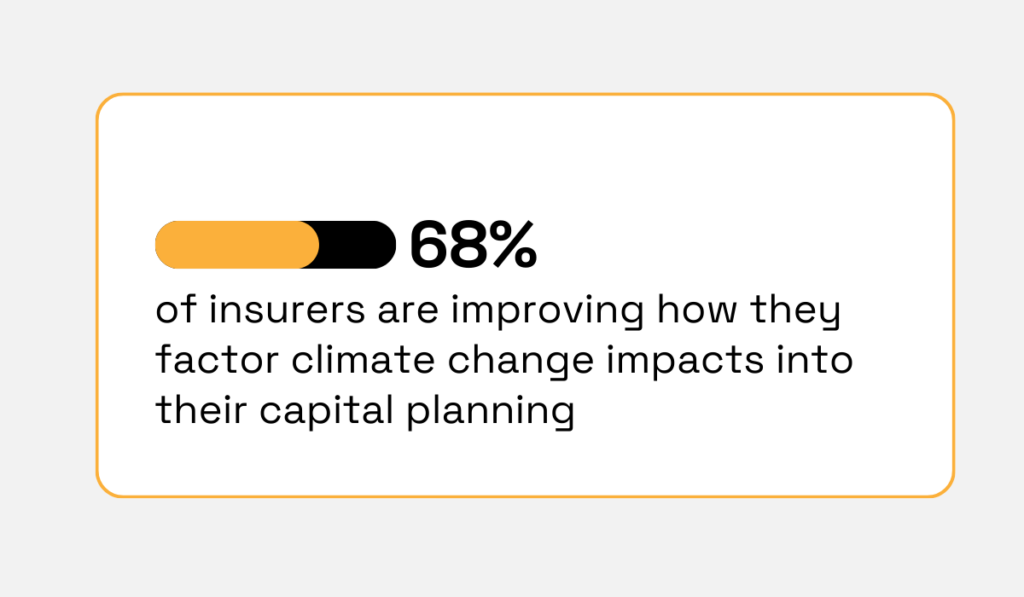

Climate volatility is accelerating this transition toward deeper portfolio insight.

Aon’s 2025 Catastrophe Risk Management Survey found that 68% of insurers are actively seeking better ways to integrate climate change impacts into their view of risk for internal capital management.

Illustration: Veridion / Data: Aon Media Room

That kind of integration is only possible when enriched data feeds consistent, portfolio-wide analytics.

Modern insurance analytics can optimize portfolio risk by providing real-time exposure insights.

For instance, you might use firmographic enrichment to track industry mix and spot emerging vulnerabilities, such as too many policyholders in a struggling sector.

This intelligence guides capital allocation and reinsurance planning. Leading insurers are already rethinking how they model and manage catastrophe exposure.

Katie Carter, Head of View of Risk Advisory for Aon in the Americas, explains:

Illustration: Veridion / Data: Aon Media Room

From what she said, aligning modeling approaches with regional risk dynamics helps insurers optimize capital usage and make stronger long-term business decisions.

Overall, enrichment powers a new level of situational awareness. That awareness starts with the quality and completeness of your data. Once those details are consistently captured and enriched, portfolio optimization becomes easy.

With a richer data foundation, you can make informed strategic decisions, including balancing portfolios, reducing unrecognized concentrations, and steering your business toward profitable opportunities.

That brings us to the end of this guide on insurance data enrichment.

We’ve explored how enriched data improves risk accuracy, speeds up operations, supports better compliance, and enables more consistent decisions across the insurance lifecycle.

When data enrichment is done right, insurance specialists start making decisions from a position of clarity and control.

Ultimately, when your data becomes deeper, cleaner, and more connected, your entire organization is better positioned to assess risk, serve customers, and compete with confidence.