Blog

Multi-Tier Supply Chain Mapping for Semiconductors

By: Stefan Gergely -

24 March 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

Key Takeaways:

Semiconductor supply chains are some of the most complex and globally dispersed in the world, yet most procurement teams still only see the first tier.

In an industry where a single disruption can ripple across dozens of countries, that’s a dangerous blind spot.

Multi-tier supply chain mapping helps you discover hidden dependencies, pinpoint risk, and make better sourcing decisions.

Here’s a practical, step-by-step guide to doing it right in the semiconductor industry.

Start by clearly defining which semiconductor components actually matter to your business.

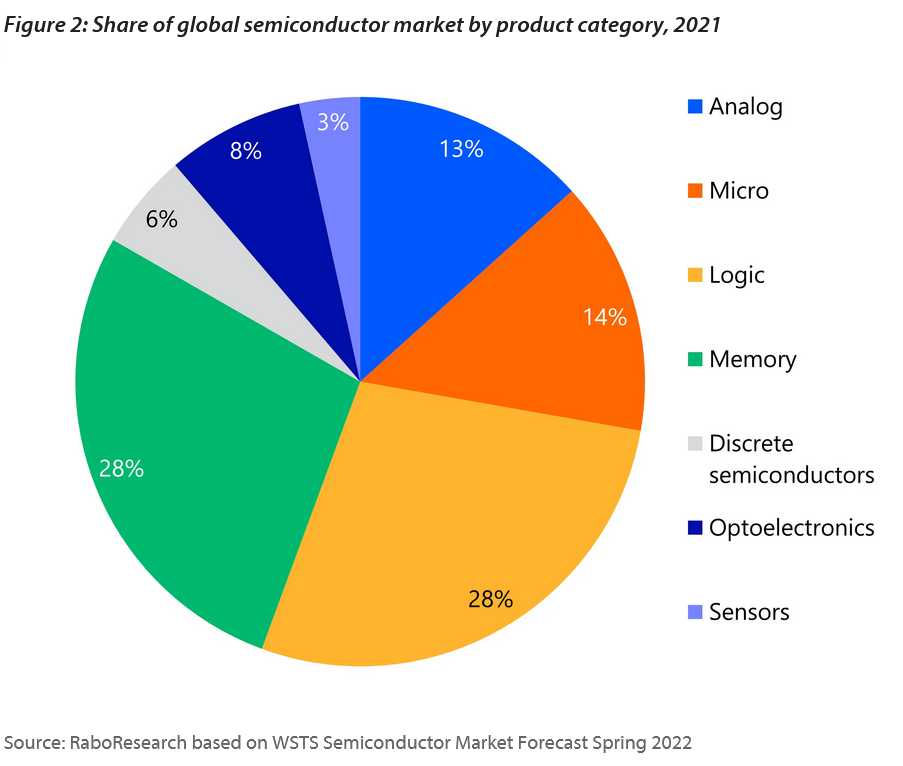

The semiconductor ecosystem is vast, spanning logic chips, memory, power semiconductors, analog devices, sensors, and advanced packaging technologies.

Source: RaboBank

Trying to map everything at once will quickly overwhelm even the most sophisticated procurement organization, so the goal here is focus, not completeness.

Begin with your end products and end markets.

Ask yourself which chips are truly critical to revenue, performance, or customer commitments.

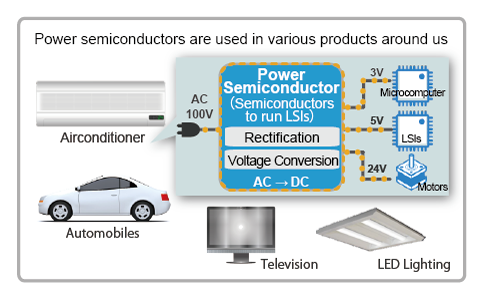

For example, an automotive OEM may prioritize power semiconductors and microcontrollers, while a cloud infrastructure provider will care far more about advanced logic chips produced at leading-edge process nodes.

Source: SanKen

These choices determine which technologies, fabrication processes, and geographic regions you need to pay attention to.

This step is especially important because semiconductor supply chains are highly specialized.

A 3nm logic chip used in AI accelerators has an entirely different supply chain, risk profile, and concentration level than a mature-node power management IC.

Source: Semidynamics

Narrowing the scope allows you to focus your mapping efforts on the components where capacity constraints, geopolitical exposure, or technological chokepoints pose the greatest risk.

Once you’ve defined which semiconductor components are in scope, the next step is to map your Tier 1 suppliers: the companies you contract with directly.

In the semiconductor industry, these suppliers typically fall into a few categories:

Check the video below to grasp the differences between them quickly:

Source: Samsung Semiconductor Newsroom on YouTube

Start by creating a comprehensive list of every supplier involved in chip design, wafer fabrication, assembly, testing, or packaging for your in-scope components.

For many enterprises, this list is spread across procurement systems, engineering documentation, and individual contracts, so consolidation is often the first practical challenge.

But as you build the list, don’t stop at company names.

You need to validate the exact legal entities you are contracting with, the contractual scope, and the specific function each supplier performs in the value chain.

This is also where major industry players start to appear.

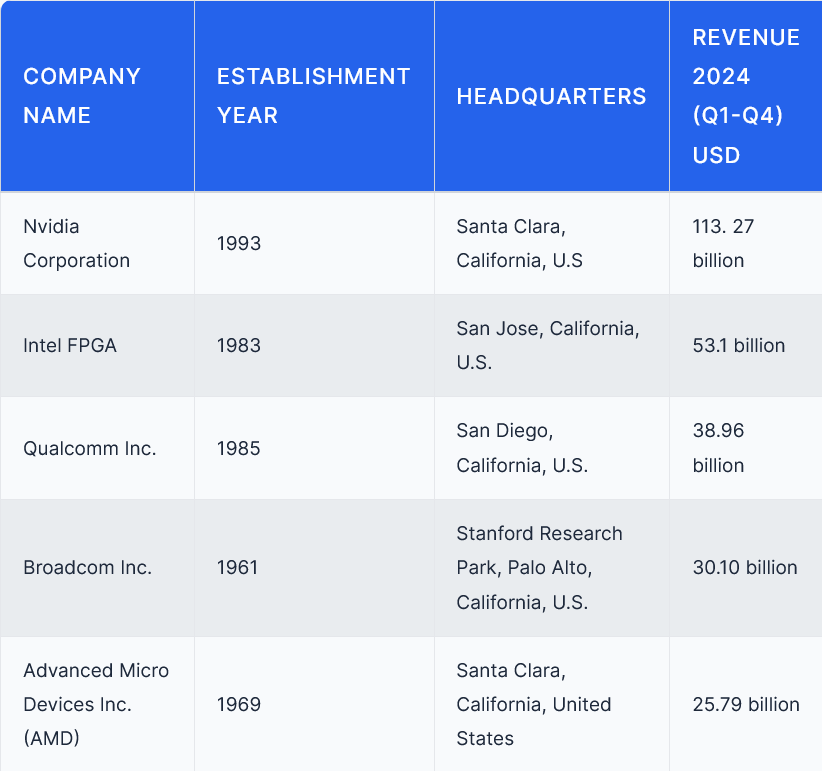

For advanced logic and AI-related chips, Tier 1 suppliers often include fabless design companies such as NVIDIA, AMD, or Qualcomm, and manufacturing partners like Taiwan Semiconductor Manufacturing Company (TSMC).

Source: Blackridge Research

In other cases, Tier 1 relationships may be with IDMs such as Intel, Samsung, or Texas Instruments, or with OSAT providers like ASE, Amkor, or JCET that handle critical back-end processes.

ASE, for example, is the world’s largest OSAT provider, and its CEO, Tien Wu, has emphasized the global nature of the industry:

“Semiconductors are relevant to everything, which is why scale is so important. A true winner must be truly global.”

Identifying Tier 1 suppliers gives you the official starting point for tracing dependencies deeper into the supply chain, but it’s important to recognize its limitations.

Semiconductor products are among the most globally distributed goods in existence.

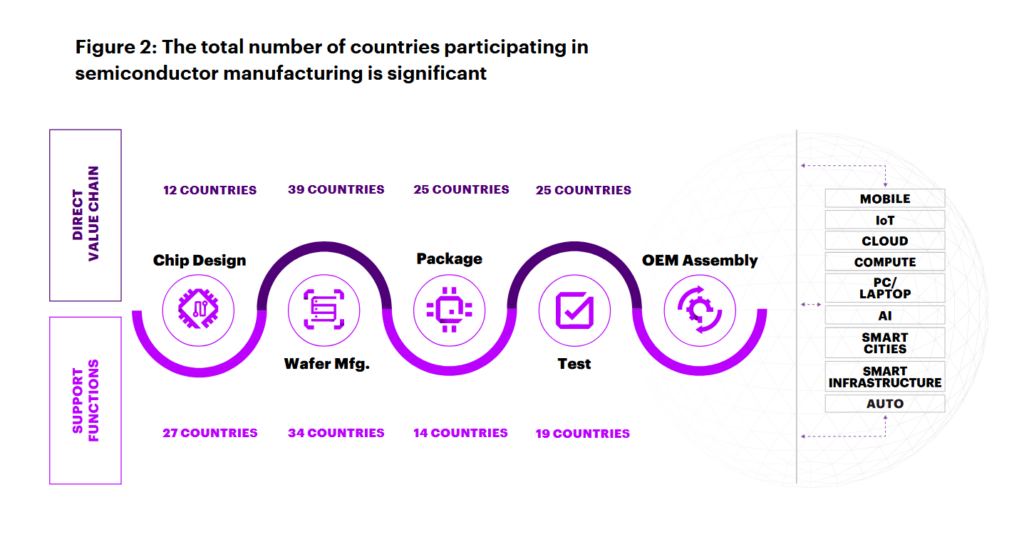

According to estimates by Accenture, the inputs required to produce a typical integrated circuit can cross more than 70 international borders before the final product reaches the customer.

Each segment of the semiconductor value chain involves, on average, over 25 countries directly and more than 20 additional countries in supporting market functions.

Source: Accenture

That level of complexity means Tier 1 visibility alone is simply not enough.

Still, when you first clearly understand who your direct suppliers are, what role they play, and how critical they are to your operations, you can establish a reliable foundation for deeper multi-tier mapping.

Without this clarity at Tier 1, any attempt to assess upstream risk or resilience would be built on shaky ground.

After identifying your Tier 1 suppliers, the next step is to map where wafer fabrication actually happens.

So, start by identifying which foundries fabricate your in-scope chips.

For each chip family, document the foundry used, the process node (such as 28nm, 7nm, or 3nm), and the physical locations of the fabs involved.

This level of detail matters because semiconductor manufacturing is not interchangeable.

Capacity at one node or fab cannot simply be replaced without redesign, requalification, and time.

This step is where many procurement teams discover that their exposure is far more concentrated than they expected.

Even if you buy from multiple Tier 1 suppliers, those companies often rely on the same small set of semiconductor foundries, process nodes, and geographic regions.

Industry data shows how concentrated this stage of the supply chain has become.

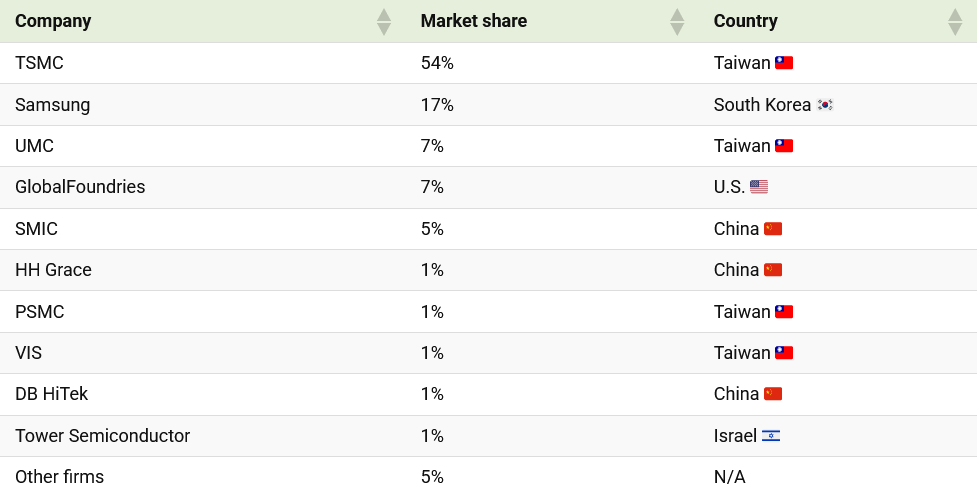

While manufacturing facilities exist worldwide, the most critical foundry capacity is clustered in a small number of countries.

In fact, four of the world’s top five pure-play foundries (TSMC, Samsung, UMC, and SMIC) are all located in East Asia.

Together, Taiwan and South Korea account for roughly 87% of the global foundry market.

Source: Visual Capitalist

Taiwan’s role is especially significant at advanced nodes below 7nm, where TSMC dominates production.

This concentration creates systemic risk.

According to research by Accenture and GSA cited earlier, wafer fabrication relies on inputs sourced from nearly 40 countries directly and more than 30 additional countries in supporting functions, from lithography equipment to fab infrastructure.

Yet the final manufacturing step itself is highly centralized.

Disruptions such as power outages, water shortages, earthquakes, or geopolitical escalation can ripple across industries worldwide.

Advanced chip manufacturing further amplifies this risk.

Producing leading-edge chips requires equipment that costs hundreds of millions of dollars per tool and fabrication plants that can exceed $30 billion in capital investment.

Only a handful of companies have the expertise, yields, and scale to operate at this level.

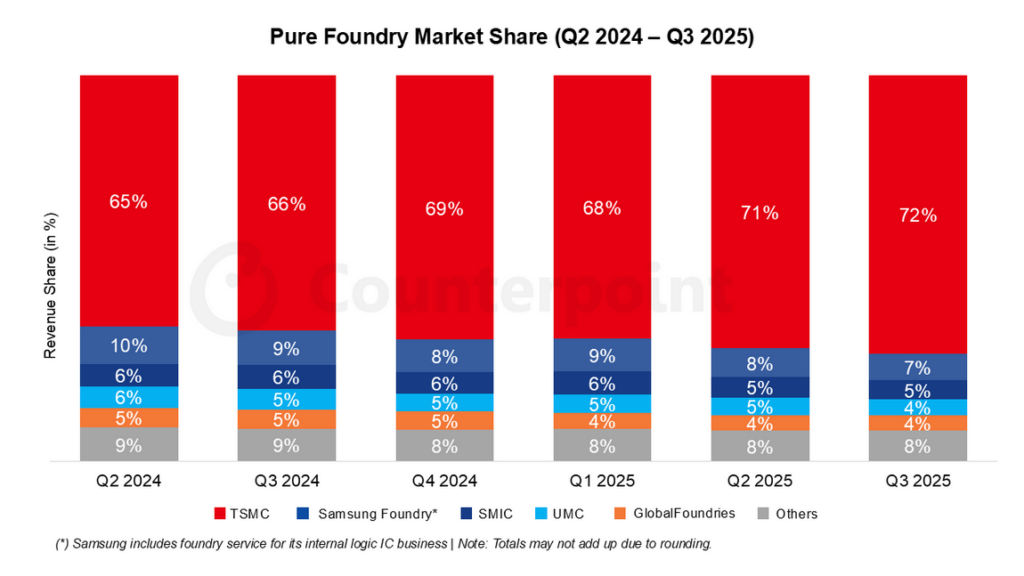

TSMC, for example, holds well over 60% of the global foundry market overall and an even higher share of advanced-node capacity.

This makes it the de facto manufacturing backbone for companies like Apple, NVIDIA, and AMD.

Source: Counterpoint

Overall, mapping fabrication dependencies allows you to quantify exposure to specific regions, technologies, and single points of failure.

When you understand exactly which fabs and process nodes your supply chain depends on, you can better anticipate capacity constraints, evaluate diversification strategies, and prepare for disruptions that may originate far upstream but have immediate downstream impact on your business.

Once fabrication dependencies are mapped, it’s time to go further upstream and look at Tier 2 and Tier 3 suppliers.

This is where semiconductor supply chains become hardest to see, and where some of the biggest risks are hiding.

At this point, you should no longer focus on chip designers or foundries.

Instead, you should look at the companies that make manufacturing possible in the first place:

These sub-tier suppliers are essential, difficult to substitute in the short term, and often controlled by just a handful of players globally.

Photolithography is the clearest example.

ASML, based in the Netherlands, is the only company that supplies extreme ultraviolet (EUV) lithography machines needed to produce advanced chips at 7nm and below.

Source: The Economist

Each EUV tool costs well over $100 million, with next-generation systems approaching $400 million.

They also take months to build, ship, and qualify.

Even if a foundry has demand and capital, it can’t expand advanced-node capacity any faster than ASML can deliver equipment.

The same pattern shows up elsewhere.

In silicon wafers, Shin-Etsu Chemical and SUMCO dominate the market for high-purity supply.

In materials, companies like JSR, TOK, and Merck provide photoresists and specialty chemicals that fabs rely on every day.

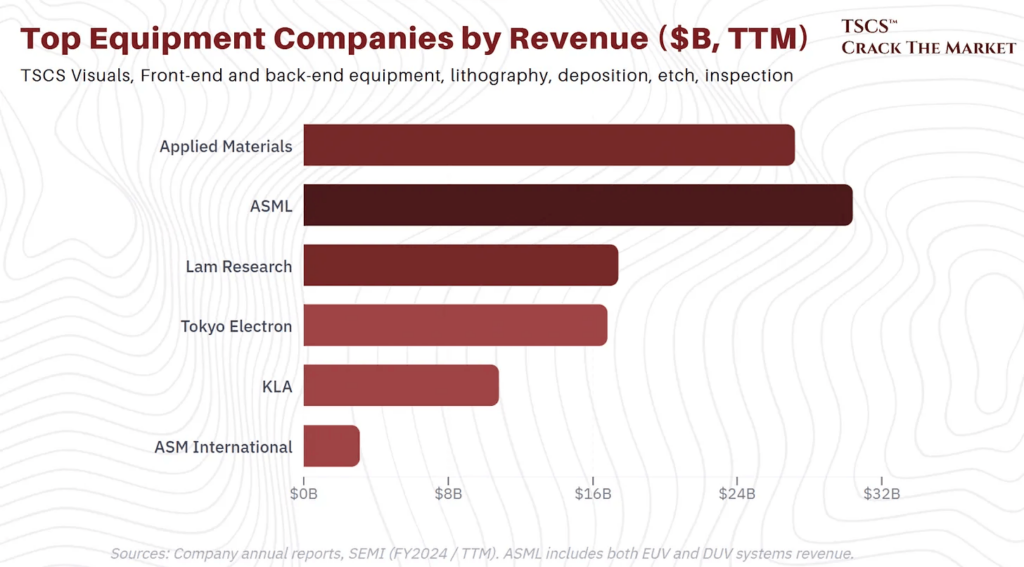

On the equipment side, Applied Materials, Lam Research, and KLA supply tools used in virtually every fab worldwide.

Source: Crack the Market

If any one of these suppliers runs into trouble, multiple foundries and dozens of downstream customers can feel the impact at the same time.

The problem is that most of these sub-tier suppliers never show up in procurement systems.

Contracts usually sit with Tier 1 suppliers or foundries, which makes it easy to assume there’s diversification where none actually exists.

Different suppliers may look independent on paper, while relying on the same upstream inputs in reality.

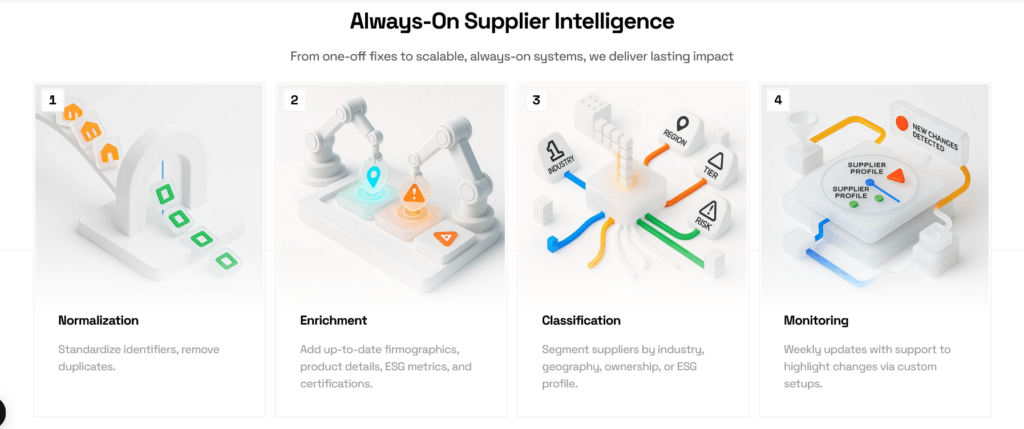

This is precisely where advanced supply chain intelligence becomes essential.

Veridion, for example, enriches and structures global business data using AI to uncover supplier relationships, operational activities, and ownership links across multiple tiers.

Source: Veridion

Instead of relying solely on declared supplier lists, organizations can see which entities are actually involved in manufacturing and how they connect across borders and tiers.

By tracing sub-tier suppliers, you move beyond a contractual view of the supply chain and toward an operational one.

That shift is critical in semiconductors, where a single upstream disruption can cascade across multiple fabs, products, and industries in a matter of weeks.

Once you have a multi-tier supply chain map in place, the real value comes from analyzing risk exposure across all those interconnected layers.

Begin by overlaying your supplier and facility data with geographic, regulatory, and environmental information.

This means mapping supplier locations and fabrication sites against risks such as:

Semiconductor manufacturing is especially sensitive to these factors.

For example, advanced fabs require enormous volumes of ultra-pure water, making droughts in regions like Taiwan a material operational risk.

Source: The Diplomat

Even short-term disruptions can impact wafer starts and ripple downstream within weeks.

Geopolitical and regulatory risk is just as important.

Semiconductor supply chains sit at the center of global technology competition, particularly between the United States and China.

Export controls imposed by the U.S. and its allies have restricted China’s access not only to advanced chips but also to the manufacturing equipment needed to produce them.

Source: Reuters

ASML’s EUV lithography systems are again a prime example.

Because ASML is the sole supplier of this technology, any change in export policy directly affects how much leading-edge capacity exists globally.

In other words, risk exposure is not limited to where suppliers operate, but also to which governments regulate the tools and technologies they depend on.

Next, look for convergence.

Even when sourcing appears diversified, the map often shows multiple Tier 1 suppliers relying on the same foundry, the same node, or the same upstream technology stack.

In a geopolitically charged environment, that convergence can quickly turn into a bottleneck if access to capacity, tools, or materials is constrained by policy decisions rather than market forces.

With these insights, you can start prioritizing mitigation strategies.

High-risk nodes in the supply chain may justify dual sourcing, long-term capacity agreements, inventory buffers, or design changes that enable the use of alternative process nodes.

Risk analysis also supports compliance and strategic sourcing decisions by helping you assess exposure to trade restrictions, sanctions, and evolving regulatory frameworks before they turn into supply interruptions.

The final step is recognizing that multi-tier supply chain mapping in semiconductors is never really finished.

The industry moves fast.

Process nodes advance, fabs expand or shut down, and suppliers adjust sourcing strategies as demand shifts.

A supply chain map that’s accurate today can quickly become outdated if it’s treated as a one-off exercise.

The recent surge in artificial intelligence demand is a good example.

In early 2026, MediaTek warned that AI-driven growth was straining the global semiconductor supply chain, pushing costs higher and forcing companies to prioritize capacity toward the most profitable products.

Source: Reuters

While the company remained confident in long-term demand, it cautioned that the supply chain would struggle to fully meet rising needs at advanced process nodes.

As MediaTek CEO Rick Tsai put it:

“With AI serving as a catalyst for industry expansion and driving the surge in demand, the global supply chain is facing challenges in fully meeting the increasing needs in 2026, resulting in higher costs across the supply chain.”

Shifts like this can change risk exposure in a matter of months.

Foundry capacity that once looked sufficient can quickly become constrained.

Pricing assumptions can break.

Upstream bottlenecks, from EUV tool availability to advanced packaging capacity, can emerge or intensify.

Without regular updates, supply chain maps fail precisely when they’re needed most.

At the same time, governments are actively reshaping the industry.

Programs such as the U.S. CHIPS Act and similar initiatives in Europe and Japan are influencing where capacity is built and how supply chains are regionalized.

Long lead times for critical equipment from suppliers like ASML further complicate planning and timelines.

To keep pace, continuous monitoring has to be built into normal supply chain processes.

You should refresh supplier data regularly, track ownership and operational changes, look for capacity expansions, and stay on top of regulatory and geopolitical developments that affect upstream dependencies.

When done well, continuous updates keep the map actionable.

They help surface emerging chokepoints early, reassess exposure as conditions change, and support better long-term planning.

Anything less than that simply won’t suffice in this demanding industry.

Semiconductor supply chains span dozens of countries, multiple tiers, and a handful of critical chokepoints.

By mapping them step by step, from defining critical components to continuously updating risk insights, you can gain the visibility needed to act, not react.

As global demand and geopolitical pressures intensify, procurement leaders who invest in multi-tier mapping will be best positioned to protect supply, manage risk, and support long-term growth in the semiconductor industry.