Blog

Why Market Intelligence Matters in Healthcare More Than Ever

By: Auras Tanase -

07 July 2026

We love our data, and now that you're here, you're one step closer to loving it too.

A wide sample of data, so you can explore what is possible with our data

Choose ->

built with procurement in mind. Focused on manufacturers, products and more

Choose ->

built with insurance in mind. Focused on classifications, business activity tags and more

Choose ->

built with sustainability in mind. Focused on sustainability commitments, and environmental and social governance insights.

Choose ->

built with strategic insights in mind. Focused on market trends, competitor analysis, and industry-specific data

Choose ->

Keep up to date with our technology, what our clients are doing and get interesting monthly market insights.

Key Takeaways:

How differently does data work in healthcare compared to other industries?

In most sectors, bad data might lead to a missed opportunity or an inefficient campaign.

In healthcare, the consequences can be much more significant.

That’s why market intelligence has become a key part of healthcare decision-making, especially in the years following COVID-19.

Read on to learn why.

Drug development is one of the most expensive activities in healthcare.

In 2025, the world’s top 16 pharmaceutical companies spent roughly $160 billion on research and development.

But spending money isn’t the hardest part. The real challenge is deciding where to invest.

Bringing a single drug from discovery to market costs an average of $2.3 billion!

That figure includes years of laboratory research, clinical trials, regulatory submissions, and manufacturing preparation.

Even after that investment, many drug candidates never reach approval.

That’s why every R&D decision carries enormous financial risk.

And the challenge is becoming even greater.

Clinical development costs continue to rise due to a combination of inflation, supply chain disruptions, and growing dependence on global suppliers.

Alexander Mirow, Head of Consulting Life Sciences at Deloitte Switzerland, sums it perfectly.

Illustration: Veridion / Quote: Deloitte

Recent events in the Strait of Hormuz show how quickly those risks can affect healthcare companies.

When tensions involving Iran disrupted traffic through the region, the impact was felt across multiple industries, including healthcare manufacturing.

Gentell, a Pennsylvania-based medical dressings manufacturer, reported raw material cost increases of up to 30%.

Shipping costs also rose sharply. The cost of moving a container from New Zealand to California increased from roughly $2,000 to $4,500.

Source: BioProcess International

These disruptions matter because many healthcare products rely on petrochemical-derived materials. In fact, petrochemicals are used in more than 6,000 everyday products, including aspirin and vitamin capsules.

So, when costs rise and logistics become less predictable, companies have even less room for expensive mistakes.

To overcome these problems, pharma companies are now using market intelligence to their advantage.

The goal is straightforward: identify weak opportunities earlier and avoid costly failures.

Take Sanofi, a French multinational biopharmaceutical and healthcare company, for instance.

The company uses predictive models to estimate how drugs are likely to perform before regulatory submission.

That single shift, paired with tighter coordination between R&D and manufacturing, is helping Sanofi accelerate time-to-market by twelve months for priority pipeline drugs, according to Sanofi’s own description of its digital and AI strategy.

A full year off a launch timeline, across an entire portfolio, is a meaningful advantage.

So, market intelligence doesn’t remove the scientific risk from R&D, but it can reduce business and market risks, and in an industry where both are incredibly high, that’s a big advantage.

Healthcare marketing has a challenge that most other industries don’t face.

A pharma company launching a new therapy needs to reach three audiences at once:

Each group responds to different information through different channels at different points in their decision-making journey.

That’s why healthcare companies increasingly rely on market intelligence when building marketing strategies.

They’re answering a different question than ‘What message do people like?’

They’re asking:

Top pharma players like Pfizer, Moderna, and more have relied on similar high-level market intelligence to plan their outreach strategies and have been quite successful, too.

Intelligence also directly affects how marketing budgets are allocated and where commercial teams focus their efforts.

For example, a company preparing to launch a new oncology therapy may discover that a small group of cancer centers accounts for a significant share of eligible patients.

Another may identify physician segments that are early adopters of new treatments and prioritize outreach accordingly.

As Amy Leonor, Vice President of Marketing at Vyne Dental, noted:

Illustration: Veridion / Quote: HealthITanswers

The broader lesson here is that market intelligence isn’t just about creating better campaigns; it’s about understanding providers, patients, and healthcare systems well enough to make better decisions before a campaign begins.

Recent FDA activity shows just how costly it can be to fall behind on regulatory compliance.

In fiscal year 2024, the FDA issued 47 warning letters to medical device companies.

That number doesn’t mean companies suddenly became less compliant.

It means regulators became more aggressive, while many organizations failed to adjust quickly enough.

Now, note that warning letters rarely come out of nowhere.

The FDA issued nearly 5,000 Form 483 inspection observations during FY 2025.

Note: A Form 483 is issued when inspectors identify potential compliance issues during an inspection. It often serves as an early warning before more serious enforcement action follows.

Being one of the most regulated industries on the planet, healthcare companies can use market intelligence to detect emerging compliance risks and regulatory trends before they become a problem.

Take the Magellan Diagnostics case

In 2024, the company agreed to a $42 million settlement after selling defective lead-testing devices without disclosing known problems.

Source: Department of Justice

The financial impact was significant.

But the damage to the company’s reputation may have been even harder to repair.

Also consider Camurus, a Swedish pharmaceutical company.

In June 2026, the FDA declined to approve its drug Oclaiz for the second time.

Source: Reuters

The reason wasn’t the drug itself. Oclaiz had already been approved in the EU and UK. The problem was unresolved quality issues at a third-party manufacturing site.

The same issue had blocked approval in 2024.

Two years later, the same site was still flagged.

The market reacted quickly. Following the announcement, analysts pushed expected U.S. approval timelines back to at least mid-2027, and Camurus shares fell approximately 7%.

It’s a powerful example of how regulatory problems can delay commercial success even when a product has already proven itself in other major markets.

To avoid such setbacks, companies can use regulatory intelligence to stay compliant, identify gaps early, and reduce the risk of penalties or enforcement actions.

Competitive intelligence is a major subset of healthcare market intelligence, helping organizations understand what competitors are developing, launching, acquiring, or discontinuing.

This is key when it comes to staying ahead, especially in highly competitive segments.

Take, for instance, the GLP-1 drugs, which everybody seems to be talking about right now.

Few rivalries in healthcare are attracting as much attention today as the obesity drug race between Novo Nordisk and Eli Lilly.

Novo Nordisk was first to market.

In January 2026, its oral Wegovy pill became the first GLP-1 pill approved for obesity in the United States.

Eli Lilly is close behind. Its competing oral treatment, Orforglipron, is expected to receive U.S. approval within months.

Source: Reuters

Whoever captures patient habit first in a category this large keeps a meaningful edge, even if a rival’s drug performs just as well.

But the obesity market is no longer a two-company race.

Several pharmaceutical companies are developing their own treatments and competing for a share of what could become one of healthcare’s largest drug categories.

WHO also points at the fact that new companies see a huge opportunity in the weight-loss market, with about 2.5 billion people worldwide classified as overweight and 890 million living with obesity.

Source: CNBC

Per CNBC, at the American Diabetes Association’s Scientific Sessions in June 2026, companies across the industry shared updates on their obesity pipelines:

There’s also a broader point worth making here.

In pharma, the window between seeing a competitive signal and being able to respond to it is measured in years, not weeks.

A Phase 1 trial visible in a clinical registry today may become a competitor launch in four years.

So companies can use competitor intelligence to continuously read the market and adjust while there is still time to respond.

Healthcare supply chains are global, complex, and vulnerable to disruption.

Market intelligence helps organizations anticipate shortages, supplier risks, geopolitical disruptions, and demand fluctuations

COVID-19 exposed how little visibility many healthcare organizations had into their suppliers, manufacturers, and logistics networks.

The OECD’s 2024 post-pandemic supply chain report documented how demand surges and border closures simultaneously drove shortages of antibiotics, anesthetics, face masks, and respiratory drugs across healthcare systems globally.

Hospitals couldn’t source PPE; vaccine makers faced raw-material shortages.

And even governments competed for the same critical supplies.

Unfortunately, those challenges haven’t disappeared.

In the U.S., active drug shortages reached a record 323 medicines in Q1 2024, affecting everything from anxiety treatments to pain management therapies.

The UK reported 135 medicines in short supply as of October 2025, while across Europe, nearly half of the surveyed countries faced shortages of 400 to 800 different medicines between November 2024 and January 2025.

Source: BBC

It’s no surprise that supply chain resilience has become a top priority.

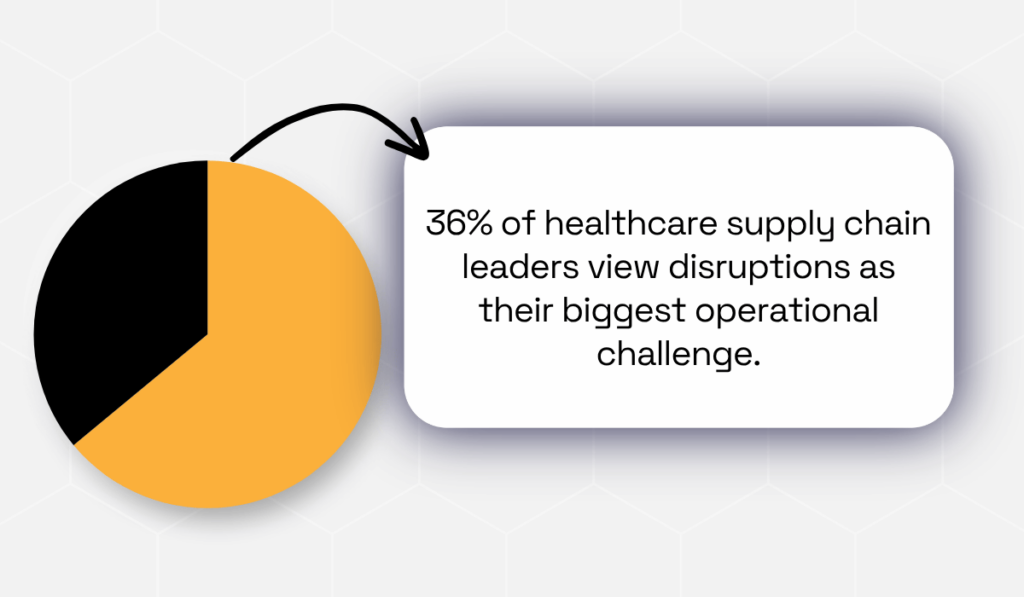

Symplr’s 2025 State of Healthcare Supply Chain Survey shows that 36% of healthcare supply chain leaders now view disruptions as their biggest operational challenge.

Illustration: Veridion / Data: Symplr

So, the question is how organizations can reduce that risk.

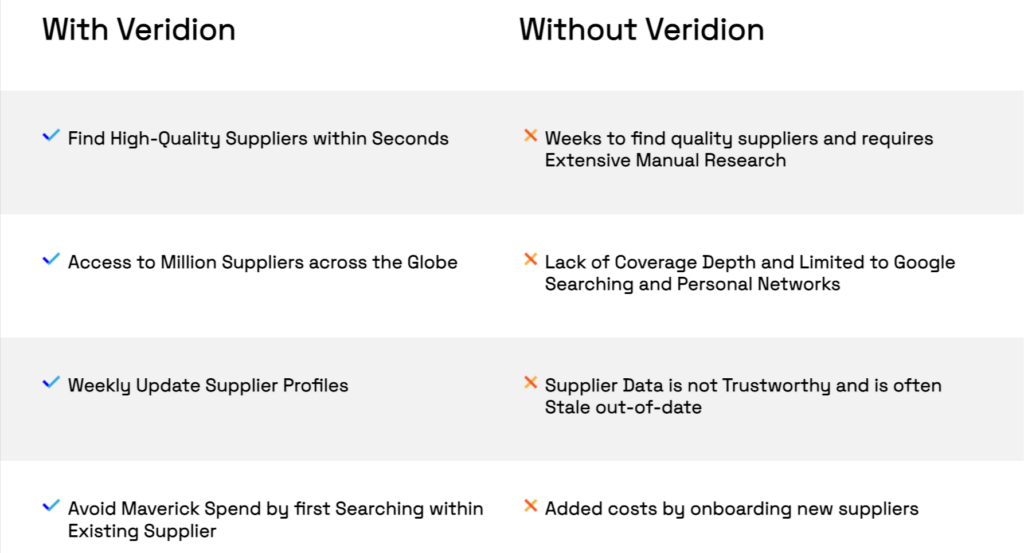

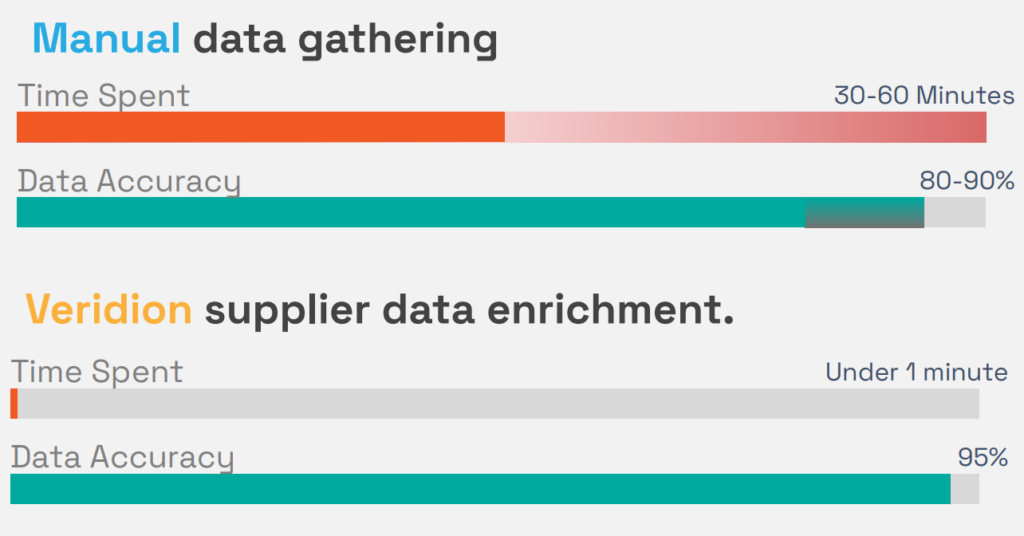

The answer starts with better intelligence. And that’s exactly what Veridion helps provide.

Veridion delivers continuously updated business and supplier intelligence across 135 million companies in more than 250 countries and territories, with data refreshed weekly and maintained at over 95% accuracy.

Source: Veridion

For healthcare procurement teams, this data can be used in two different ways.

The first one is supplier discovery and diversification.

Instead of waiting for a shortage to occur, teams can identify qualified alternative vendors based on product category, geography, industry, and compliance requirements ahead of time.

This allows organizations to build resilience before disruptions impact operations.

The second is supplier monitoring and third-party risk management.

A change in ownership, financial health, operational status, or business activity can create vulnerabilities that affect the entire supply chain.

With continuous monitoring, those changes can be identified early rather than after a disruption has already occurred.

Source: Veridion

Veridion automatically surfaces these updates, helping procurement teams stay informed without relying on manual checks.

Each company profile contains more than 320 business attributes, including ESG indicators, location intelligence, product and service data, and corporate hierarchy information.

That level of market intelligence gives procurement teams a much deeper understanding of their supplier ecosystem.

And when the next supply chain disruption arrives, they’re not starting their search for alternatives from scratch.

The decisions that matter most are also the ones that are hardest to make without good data.

Where to direct R&D spend. How to effectively reach patients and providers. How to stay ahead of the regulatory curve. What competitors are doing before it shows up in market share. Whether your suppliers will hold up under pressure.

Healthcare has always rewarded organizations that use market intelligence to plan ahead.

The organizations building that capability now, across R&D, marketing, compliance, competitive strategy, and supply chain, are the ones that will find the next five years more navigable than the last five.