Measuring cost savings is a significant metric for the procurement department.

It’s the litmus test for cost-saving strategies like strategic sourcing or tech adoption that shows whether or not these strategies bring tangible financial benefits to procurement.

Today, we’ll break down why you must track cost savings in procurement and how you can do it.

We will also shed light on savings tracking methodology and how to navigate the reporting of this metric to other stakeholders.

Let’s dive right in.

Understand the Main Concepts in Tracking Savings

Let’s face it—procurement cost savings is a broad term, and if you don’t fully grasp it, you can get misleading data on how much you save.

That’s why, before diving deep into the topic, we must first clarify some of the main concepts in tracking savings.

Addressable Spend

The first concept to consider is addressable spend , or the portion of your total spending that is open to cost-saving strategies.

Clearly defining this spend is necessary because if you don’t, you won’t get accurate information on how much you saved.

For instance, if your company’s total spend is $500 million, with $5 million in procurement savings, claiming a 1% saving is misleading.

Non-addressable spend, like utilities, payroll, taxes, and other non-negotiable expenses, must first be subtracted from the total spend to reveal the true addressable spend.

Only then can you get an accurate savings percentage.

Cost Savings

Procurement cost savings represent the actual monetary gains resulting from implemented cost-saving strategies.

They are tangible expense reductions that you see on financial statements and are the results of price negotiation, process optimization, technological integration and other cost-saving initiatives.

These are also the savings that your finance department colleagues are most interested in.

Cost Avoidance

On the other hand, cost avoidance emphasizes proactive measures to prevent unnecessary costs.

It involves anticipating potential expenses and taking steps to mitigate or eliminate them.

Cost avoidance can be realized through risk mitigation strategies and adding value-added services, which makes it a forward-thinking approach for long-term economic responsibility and resilience in procurement.

However, to calculate cost avoidance, you must estimate the hypothetical costs that were prevented, which makes it much more difficult to measure.

Still, you can’t gain a whole financial picture of your procurement without taking cost avoidance into account.

Expected vs. Realized Savings

Distinguishing between expected and realized savings is also crucial.

In a nutshell, expected cost savings are the projected financial benefits set before implementing procurement strategies, while realized cost savings represent the actual outcomes achieved after the strategies have been put into action.

Monitoring both aspects will allow you to measure the success of your procurement efforts and make informed decisions for continuous improvement.

Choose the Tools for Tracking Procurement Cost Savings

To effectively track cost savings in procurement, you must first choose the right tools.

The tools in question are spreadsheets like Excel or different types of modern software.

Excel is probably one of the tools you widely use in your organization, and partly also for tracking savings.

But is it really such a good option for measuring savings?

While it may be a familiar and accessible option, allowing you to deal with many subjects, you may find handling large datasets and conducting complex analyses challenging in Excel.

Also, with manual data entry, you increase the likelihood of errors, and because of the sheer volume of Excel spreadsheets, you can have difficulty locating those errors.

Additionally, Excel lacks the advanced features that modern software has, restricting its capacity for in-depth procurement analytics.

Considering these drawbacks, choosing modern software alternatives for tracking procurement savings is much wiser.

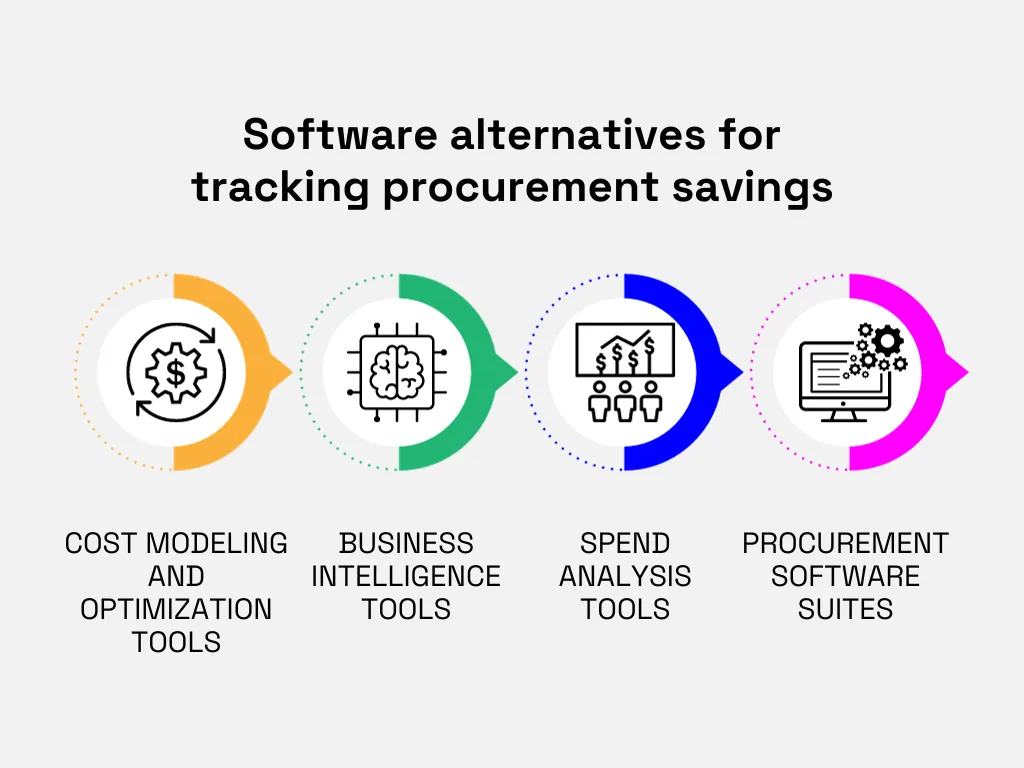

Let’s go through the most useful ones designed for this purpose.

Source: Veridion

Cost modeling and optimization tools allow you to systematically track your procurement savings by analyzing and optimizing expenses.

These tools can also provide a clear overview of your spending patterns and identify areas for cost reduction.

One such tool is ProPurchaser, designed to provide precise price benchmarking, advanced cost modeling, and tailored negotiation strategies based on tracking commodity drivers.

It works on the following principle :

We track commodity cost drivers that affect suppliers’ production costs and alert our members as changes occur. When suppliers’ costs fall, our members use this information to negotiate lower prices; when costs rise, they fend off unsupportable increases.

Business intelligence tools, such as Qlik and Looker, are also efficient in tracking savings.

These tools integrate with diverse procurement data sources, providing advanced analytics and comprehensive reporting.

Business intelligence tools also feature user-friendly interfaces and interactive dashboards for accessible data interpretation beyond basic tracking.

So, they are great (and highly needed) when reporting data to other stakeholders.

Source: G2

Of course, tracking savings wouldn’t be possible without dedicated spend analysis tools.

Such tools will help you examine your spending patterns to understand where your resources go.

Spend analysis tools excel in identifying areas for potential cost savings and optimization, contributing to your overall visibility into procurement spend and improving data-driven decision-making.

Finally, you can opt for comprehensive procurement software suites.

Procurement automation software , like SAP Ariba and Coupa, covers various aspects of the procurement lifecycle, integrating features such as spend analysis, contract management, supplier management, automating invoicing, and more.

Moreover, through analytics and reporting features, such software suites allow you to monitor and assess cost-saving initiatives, track negotiated savings against actual spending, and generate comprehensive reports that show your procurement performance.

Source: Coupa

The choice of tools for tracking procurement cost savings depends on the specific needs and goals of your procurement, as well as the volume of your purchasing.

While Excel may suffice for basic savings tracking, modern software alternatives offer advanced features tailored to complex procurement demands.

Such software will also measure your savings more accurately and help you identify additional cost-saving opportunities.

Formalize Savings Tracking Methodology

You can’t start measuring cost savings in procurement without first establishing and formalizing a savings tracking methodology.

In essence, this means addressing key questions that define the scope and parameters of your savings measurement process.

The first step is establishing a clear baseline, a reference point to gauge how much money is being saved.

However, according to Collins Oluka, the head of global procurement at Velcro companies, it’s crucial to secure enterprise-wide consensus on this baseline.

Only when there is collaboration between the chief procurement officer and chief financial officer and when they agree on a baseline can you accurately measure cost savings and track the real impact of cost-saving initiatives.

The baseline can be your historical data, industry benchmarks, or budgeted allocations.

Depending on this, you can use different models to measure cost savings, which we will focus on in a few moments.

Then, clearly define what aspects of procurement you will measure.

Will it be savings per product, per supplier, or per category?

Are you going to focus solely on cost reductions, or will you also measure cost avoidance?

This will also influence how often you measure savings.

For instance, if you want to measure the success of cost avoidance strategies, you have to do it annually because, unlike cost savings, the results of cost avoidance efforts may become more apparent over an extended period.

Once you address all these questions and establish a methodology framework, you can start measuring your savings through different models:

Historic Savings

Through this model, you essentially compare new and old costs and savings achieved compared to the past.

You can achieve such savings by renegotiating prices with suppliers or sourcing new suppliers to purchase the same products or services.

Let’s say supplier A traditionally provided a component at $10,000 per unit.

However, you improved your sourcing by using sourcing tools like our Veridion , and discovered supplier B that offers the same component at $8,000 per unit.

Source: Veridion

In this case, you would realize a historic saving of $2,000 per unit, calculated as the difference between the old and new costs.

However, you can apply this method only when you compare prices of the same components. If you compare apples and oranges, you won’t get accurate cost-saving results.

Budget Savings

Budget savings involve comparing your planned budget with actual spending.

If your budget allocates $100,000 for a specific procurement, but you end up spending only $80,000, the resulting budget savings amount to $20,000.

This model helps evaluate fiscal discipline and efficiency in budget management.

However, your planned budget has to be realistic to measure accurate budget savings.

RFP Savings

Request for proposal (RFP) savings are derived from the competitive bidding process.

By sending out proposals and selecting the lowest bidder, you quantify savings achieved through efficient negotiation.

For instance, if the lowest bid is $50,000 compared to the next highest bid at $60,000, the RFP savings amount to $10,000.

But when it comes to competitive bidding, you shouldn’t always go with the lowest bid.

In fact, you should prioritize factors like delivery times, added-on services, and product quality.

To put it plainly—if you end up going with the lowest bid but don’t take these into account, you will, in the long term, end up with more additional costs than savings.

Technical Savings

You can realize technical savings when you choose to procure alternative products or services with different technical specifications.

Consider a manufacturing company producing custom metal brackets.

Let’s say they originally cut from 120 x 80-inch metal sheets, but when they review the process, they reveal that cutting from smaller sheets is equally efficient without compromising quality.

By modifying technical specifications and procuring smaller metal sheets, they can achieve significant cost savings not only in terms of lower prices for smaller sheets but also by reducing material wastage and lowering the cost per bracket.

Using smaller sheets can also lower transportation costs by reducing space requirements during shipping.

Technical savings would then be calculated as a difference between the original metal sheet cost and a smaller metal sheet cost.

However, adjusting technical requirements has to be decided with all stakeholders involved.

Index Savings

Index savings involve monitoring changes in costs due to internal market developments.

Let’s take an example of managing its IT software licensing costs.

Say that the industry trends project the annual inflation rate for software licenses to be 8%.

However, the organization, in alignment with its strategic goals, sets a target to cap cost increases at 5%.

If a software vendor increases their subscription by 4%, traditionally, it might be seen as a cost rise.

Yet, within the framework of index savings, this is considered a saving because they didn’t go above 5%.

This model aligns procurement practices with broader economic conditions and benchmarks.

Ratio Savings

Ratio savings represent a combination of previous models. Let’s take an example of technical and budgetary savings.

If the budget allocates $1,200 for a specific technical product but by changing technical requirements, you procure an alternative product for $1,000, you can realize both technical and budget savings.

Decide What Data to Report On

After measuring your cost savings through these models, the next crucial step is determining how to handle this data—to whom you will report it, how you will present it, and how frequently.

Reporting is one of the most important aspects of cost savings measurement as it bridges the gap between the measured data and the understanding of its impact on cost savings for management and other stakeholders.

Given the diverse needs and expectations of different stakeholders regarding cost savings, it is essential to tailor your reporting approach to meet those specific requirements.

Here is a table summarizing the reporting recommendations for different stakeholders within a company, including the data focus, reporting frequency, and preferred reporting format:

Stakeholder | Data focus | Reporting frequency | Format |

Financial department | Hard savings immediately visible in financial statements | Frequent reporting recommended | Detailed reports on quantifiable savings achieved through procurement |

Executive management | Insights into both hard and soft savings | Quarterly or biannual | Comprehensive reports presenting a holistic view of procurement impact |

Other stakeholders | Customized reports based on departmental spend and savings requirements | Tailored to specific needs | Reports addressing unique requirements of different departments |

Considering the dynamic nature of procurement, reporting should encompass planned and realized savings.

This will give all stakeholders a comprehensive overview of the strategic goals and the achieved outcomes, fostering transparency and accountability.

When presenting the data, you should frame it within the context of procurement cost-saving strategies and emphasize their alignment with organizational objectives.

Also, make sure to use charts, graphs, and other visuals to enhance the clarity and impact of the data.

Unlike plain text and numbers, a visual representation will allow all stakeholders to quickly and more profoundly understand the reported metrics.

Source: Veridion

In summary, effective reporting in procurement involves a tailored approach that considers the distinct needs of different stakeholders.

So, make sure to present data in the context of cost-saving strategies, turn it into captivating visuals and help everyone understand how significant procurement is for realizing cost savings.

Why Measure Your Procurement Savings?

Now that we’ve explored the intricacies of measuring savings, let’s round out this article with one last question—why do it in the first place?

As we have seen today, measuring procurement savings is crucial because it provides a concrete way to assess the effectiveness of your cost-saving strategies.

It is a reliable key performance indicator, offering insights into achieved savings and avoided costs.

If, by measuring cost savings, you learn that your strategies yield results—keep up!

Conversely, if the results are not as expected, it signals the need to reassess and adjust your cost-saving strategies.

Source: Veridion

Beyond assessing strategy effectiveness, measuring savings also:

- Enables a comprehensive evaluation of overall procurement performance.

- Informs decisions on whether to sustain or modify existing strategies.

- Serves as a foundation for refining and improving cost-saving approaches over time.

All in all, measuring procurement savings is not just about quantifying immediate financial gains.

It’s also a strategic tool for informed decision-making and ongoing improvement in managing your resources.

Conclusion

Measuring cost savings in procurement is by no means an easy task. On the contrary, it requires good preparation, well-structured methodology, and proper tools.

However, once you start measuring cost savings in procurement, you will be able to see if your procurement cost-saving strategies yield results.

The insights you get will guide you to make informed decisions, continuously improve your procurement processes, and pave the way for continued cost savings.

Articles

Discuss how these trends affect your organization.

Our analysts are available for a short call. Bring a specific question and we will ground it in the data.